I am sure, all of you, reading my blog, have a portfolio of insurance, savings and investment policies.

Some of you, may have a manageable 3 or 4 policies. While some, have more than 10. My question to you right now is,”Do you know EXACTLY what you are having?”

Do you know, when you can claim and when you cant from your insurance policies?

Do you know, whether if your critical illness coverage is enough and what is the shortfall?

Do you know, how much you need for your retirement, child’s education and the shortfall/excess that you have?

…or simply put across, do you know, what is the PURPOSE of you getting the policies that you currently have???

The only solution to these, is having YEARLY FINANCIAL REVIEWS.

In a span of 2 weeks, I met 2 clients with tragic stories…

1) Father In Law Cannot Claim Hospitalisation Insurance plan

I did a financial review for my client just now. She also brought her father’s in law policy from a different company, for my interpretation.

She asked me, “My father in law going for heart by pass surgery next week. I check with the claim’s department of X company…They say cannot claim…Can you interpret the policy document for me?”

I interpret for her, realising while the policy owner of the hospitalisation plan is her father in law, the insured is her MOTHER IN LAW… Her father in law does not have any hospitalisation coverage.

………………………………………………………………………………………………….

2) Client and his family think he got a death coverage of $300,000

Last week, I met my prospect at his home and he get hospitalisation plans for himself and his family.

I enquired him on his coverage, in case, death, total and permanent disability or critical illness were to strike. How much will his wife, 2 sons and 1 daughter get?

He looked at me confidently and said, “No worries. Anything happen to me, my family will get $300,000…”

I felt relieved, because, as he is earning a takehome pay of $2,500/mth, $300,000 will be adequate. Nevertheless, I asked for all his policy documents for me to help him “refresh” on the existing plans he has.

To my surprise, I realised he only have $30,000 of coverage in case of death. His family will only get $300,000 if he DIED DUE TO ACCIDENT…

You can imagine, the look at his face…For many years, he has been telling his wife, in case of death, “you will get $300,000″….

Call me up at 96520134. Let me help you…Insya’allah… 🙂 🙂 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

Everyone in the globe dreaded this “outflow” called TAX.

This is my first time, I pay tax to the government…. and due to my hectic schedule (going for seminars, doing roadshows and meeting clients), I “forget” to make the payment.

They send me a letter, saying that I will be fined extra $28.10. However, because this is the first time, I am paying tax, they will waive it for me if I make the payment by 9 July 2009.

I did it on that very day, using AXS machine. (Victory Sign) 🙂 🙂 🙂

Btw, I’ve been brainstorming ideas, ways and methodologies where YOU CAN REDUCE YOUR TAX PAYABLE OR PAY 0% TAX IN SINGAPORE LEGALLY!!! (evil but innocent smile..hehe)

Note: The strategies that I am going to share with you is purely legal and ethical. (Information accurate as at 23rd July 2009)

Strategy #1) If you are employee,sole proprietor or in partnership, you just need to ensure that your chargeable income (income that is liable for tax) is less than $20,000, and you DONT HAVE to pay any taxes.

Chargeable Income = Total Income – Tax Allowable Expenses – Tax Reliefs

In Singapore, an average Singaporean brings home, disposable income (money that go inside your pocket) of about $5,000/mth or $60,000/year.

So, the first method is quite difficult to apply. Yet , YOU CAN ALWAYS REDUCE YOUR CHARGEABLE INCOME, by documenting and declaring your tax allowable expenses.

Tax allowable expenses are expenses incurred in order to GENERATE income.

Example, if you are a financial consultant like me. Document your roadshow costs, cost for printing namecards, cost for knowledge upgrading like going for seminars and other expenses related to helping you GENERATE your income.

When your chargeable income is lower, you pay lower tax, or no tax if your chargeable income is less than $20,000.

………………………………………………………………………………………….

Strategy #2) Claim as much “reliefs” as you can.

The first relief that every working Singaporean has is Earned Income Relief.

Earned Income Relief reduces the amount of Chargable Income, thus reducing the amount to be taxed.

Below 55 years of age $1,000, 55 to 59 years of age $3,000, 60 years of age onwards $4,000

Strategy #3) Contributions to CPF helps you to save tax

When you contribute your CPF, you can also reduce your tax.

Right now, you are required to contribute 20% of your salary to CPF and your employer pay 14.5%.

You can only get the money when you reached age of 55.

Example if, you earn $2000/mth.

$400 of your pay is going to CPF. You take home only $1600. You only need to pay tax for your take home pay of $1600. Money that goes to CPF is not taxable.

Supplementary Retirement Scheme is a savings plan that you can sign up when you reach 21 years old.

You can contribute up to 15% of your income. You can use this money to offset your total income, thus reducing your chargeable income.

(Btw, if you already have an SRS account, I can help you get BETTER returns, then leaving it there. Call me for appt! ).

…………………………………………………………………………

Strategy #5) Capital Allowances

The assets you buy for your business operations can be used to reduce your tax.

The assets you buy, depreciates in value every single year. Depreciation is an expense and thus tax deductible. The $$$ that you can use to write off differs than accounting term.

Accounting depreciation, takes into account the life of the assets you buy till it become scrap or ready to be disposed.

Depreciation or capital allowance for tax purpose is STANDARDISED!

Example: Computers, hardwares and printers, take 1 year to write off

Plant and Machinery, take 3 years to write off.

Commercial vehicles, take 6 years to write off

Example, for me, I buy laptop, printers etc2 for my business operations..If my laptop and printer cost, example $3000, I can just classify $3000 as my capital allowance and deduct it from my total income, thus reducing my chargeable income.

There are really many ways (like donations to approved charities, paying insurance premium etc2), that you can use LEGALLY, to reduce your tax. It requires planning and continual education.

Hope the above information helps!!! 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

There is a Malay proverb that says, “Melentur buloh, biarlah dari rebungnya”…

Translation: “If you want to carve bamboo, carve it from its base”

I firmly believe that, if you want to teach your child something GOOD… you better teach them when they are still YOUNG….this is BECAUSE, when you teach them when they are still young, they will LIVE TO REMEMBER!!! 🙂

One of the things, that, parents NEED to share with your child is, the HABIT OF SAVINGS…

I remember, when I was in primary school, I have this big, big transparent savings tin in my room. My mother gave me $0.50 of pocket money each day, and I will diligently put in $0.10 every day. (that’s 20% savings)

I continue, to do so until it become a habit. A habit which I continue to practice till today…. 🙂

Another habit, which parents need to preach to their child (notice, I use the word preach) is BUY only when you can AFFORD. I realised, while doing fact finding with clients in roadshows, that many youngsters today having credit card debts.

That is not healthy and never it will be healthy….@ 2% interest per month, 24% interest per year…The interest is simply too much… 🙁

Inculcating that habit of “BUY only when you can AFFORD” is extremely crucial…

Okay…Now, you may be telling me….”Helmi, we already know the importance of savings blablabla…….So, what is the best methodology to teach OUR children these good MONEY values….???”

Simple…..Its by preaching….You do it, and they follow.

If you want your child to love reading, you too need to love reading books. You need to show them, prove to them with your actions that you LOVE reading books.

If you want your child to love to eat vegetable, you too need to show your child that you LOVE to eat vegetables. You need to show them, prove to them with your actions that you LOVE eating vegetables.

If you want your child to love to SAVE money and not spend lavishly, you too need to show your child that you LOVE to SAVE money and not spend lavishly. You need to show them, prove to them with your actions that you LOVE to save money and not spend lavishly.

So remember…The way to share with your children GOOD money values is by “preaching” and not by “teaching”….

Show them, lead them as an exemplary model. When you teach, you may be doing the exact opposite. (Example, you watch TV while your child is busy studying)

BUT when you preach, you walk your talk and substantiate your beliefs with actions. Actions speak louder than words.

All the great successful people on earth are great “preachers” and not “teachers”..

Example, Prophet Muhammad SAW, Mahatma Gandhi, Barack Obama…..

So remember….Preach your child of good money values, and they will heed your advice!!! 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

I am very sure, you heard before, the 8th Wonders Of The World, which is “COMPOUND INTEREST”… as mentioned by Albert Einstein, the scientist who is famous for his theory of relativity.

…………………………………………………………

View this video, to see a simple explanation of how compound interest can help your money grow over time. 🙂

There’s a saying that if you FAIL to PLAN, then you PLAN to FAIL.

If you do not even care to plan, you will then be automatically be part of other people’s plan.

In todays’ context, I will be touching on creating your own financial plan. There are 6 Steps altogether, to build your personal financial plan. 🙂

Step 1- Set Goals and Objectives

What exactly do you want? You want to accumulate money for retirement? You want to accumulate money for your child’s education?

…or simply you want to leave some money for your beloved spouse and children, in case you go to heaven the next day?

Identify and segregate your goals, into SHORT TERM goals, MEDIUM TERM goals and LONG TERM goals! 🙂

…………………………………………

Step 2- Gather Data

Before you go to war, you need to know what weapons, do you have… the number of soldiers available and more relevant information.

Similarly,when you want to devise your own personal financial plan, you need to take stock of yourself financially. Where are you now?

Create your own net worth statement and cashflow statement.

……………………………………………………………………………………….

Step 3- Analyse and find solutions

So…you have consolidate your financial data into relevant structures like networth statement and cashflow statement? It is time for you to interpret them.

Benchmark it to your goals. How far off you are from your goals? What are the solutions and alternatives involved? 🙂

…………………………………………

Step 4- Recommendations

Out of the solutions and alternatives, CHOOSE the best one, most suitable for you. If you are super risk averse, investing in funds, will not be an option for you. You will love super safe, guaranteed endowment plans.

Relatively, if you are the gung ho and dare to take calculated risks, investing in funds will APPEAL to you. You may view, the returns from endowment plans as too little.

CHOOSE the best options for yourself.

…………………………………………

Step 5- Implementing Strategies

After deciding, which strategies suit you most, it is time to IMPLEMENT them.

…………………………………………

Step 6- Follow Up and Annual Reviews.

Every year, there will be changes in your family. Perhaps, if you are single, you may be getting married. If you are married, you may now have a newborn child. If you are working, you may now be enjoying a pay raise.

So, it is therefore, crucial for you to do an annualized review on your financial plan. What needs to be changed? What needs to be removed or add on?

Btw, if you need any help in the construction of your financial plan, you can always call me, Helmi Hakim at 96520134, for me to assist you in the creation and development of your financial plan. See ya! 🙂 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

A recent survey by OCBC bank found that 6 out of 10 parents save only up to $40,000, when planning for their child’s tertiary education.

This statistic is NOT SURPRISING.

During the fact finding process I’ve done for my clients, I analyzed that many have a number of endowments or investment linked plans and they feel contented….. with what they have….without realizing their shortfall.

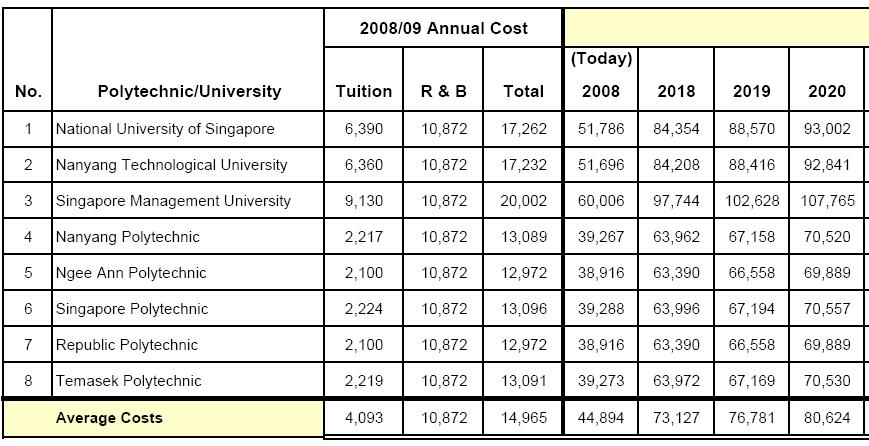

If you have a 10 year old child, who intends to go to a local university like NUS,SMU or NTU in the future, he will need at least $84,000. If he CHOOSES to study abroad, the amount will snowballed.

I will not indulge in an open discussion on best methdologies one should adopt to accumulate their child’s education funds’, because every individual has their own risk profile. You can contact me personally, for a non obligatory discussion in my office.

What I am trying to bring about here, is the awareness of knowing what plans you have and how it will impact you. Hiding behind that contentment, “I already have savings for my child’s education” wont help, if really, the projected amount for that upcoming years is relatively inadequate.

Start planning now! Your child’s future is in your hand! 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

A certified financial consultant, Helmi Hakim has won praise for his patience, perseverance and practicality when solving his clients’ financial concerns. For more information on how you can manage your finances better, contact Helmi Hakim at 96520134.