One of my favourite topics is on retirement planning.

Recently, a lot of people came to me asking for tips, strategies on how they can save money for their retirement.

In this blog post, I will share with you, 5 Most Important Rules To Halal Savings For Your Retirement In Singapore…

…………………………….

……………………………

…………..

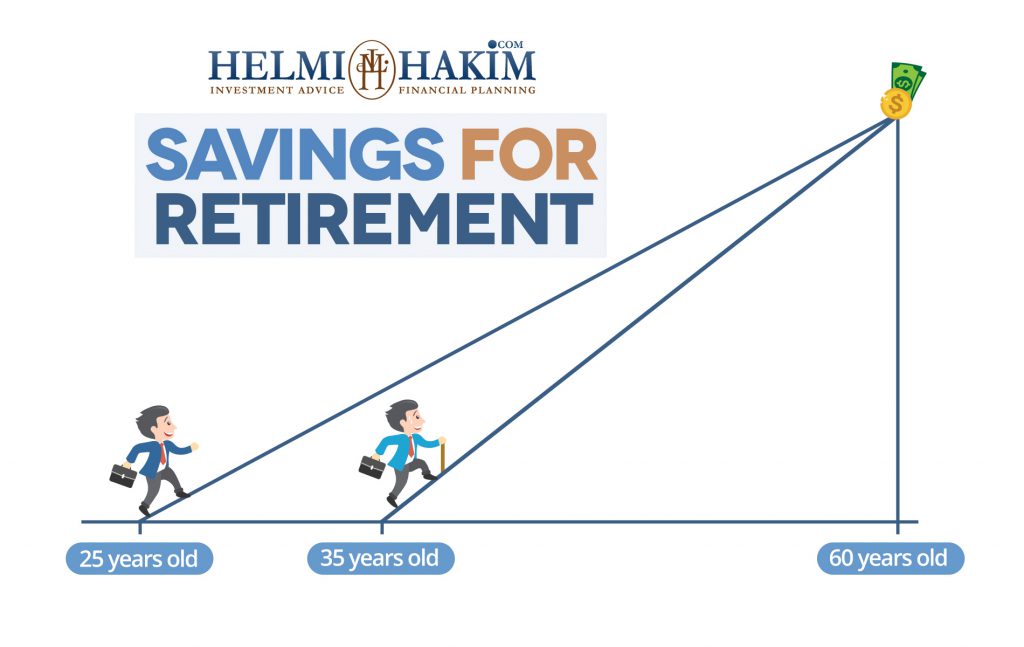

Rule #1. Start Early

This is my story.

During my early years as a financial consultant, I always advise my clients of the importance and advantages of saving money EARLY for their retirement.

Yet at times, I myself faced challenges when I wanted to save money. I came out with lots of “EXCUSES”!

……………………………………………….

………………………..

“Alah… Wait lah… Im still young. YOLO!!!!

Enjoy first. Later, when I am in my thirties, then I will start saving for my retirement.”

“Alah…. My pay is so little now. Wait when my income increases to a substantial amount, then I will start saving for my retirement.”

………………………………………………

………………………..

Yet deep down in my heart, I know that the best time for me to start saving money for my retirement is when I step into the workforce.

This is because, at that point of time,we DO NOT have high money commitments.

We don’t have a wife to give nafkah.

We don’t have children to provide for their daily living expenses.

We don’t have a house to pay for monthly mortgages.

…………………………………………

……………………….

The facts and figures are as clear as daylight.

If you want to retire comfortably in the future.

No shortcuts! Start saving money for your retirement as EARLY AS POSSIBLE!🙂

(The hill gets steeper if you choose to procrastinate and delay your savings for your retirement)

…………………

…………

Rule #2. Follow A Proven System and Personalize It

As you know, I struggled to save money during my early 20s.

Yes. I had my savings account. (I opened one at that point of time because I knew the importance of saving money for rainy days. In Malay, we call it, ‘Sediakan payung sebelum hujan’)

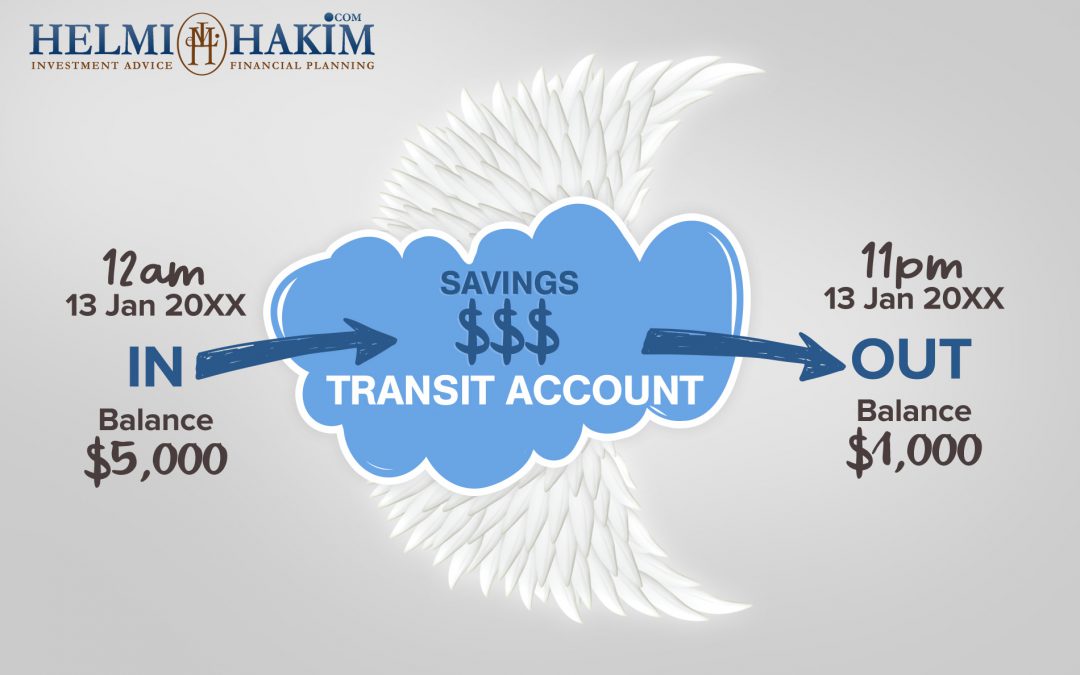

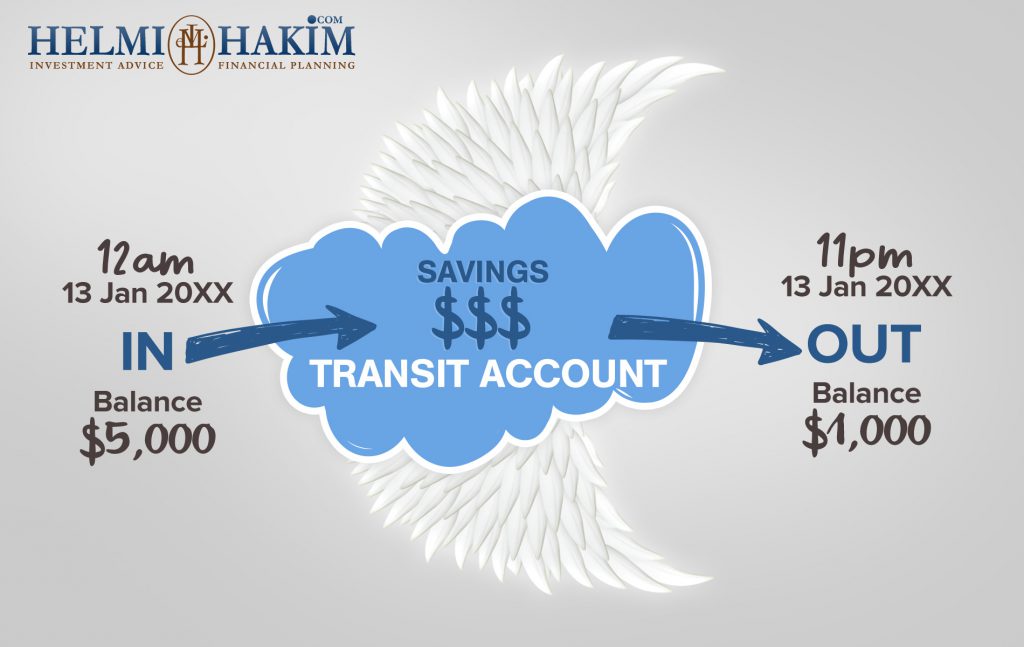

Yet. My SAVINGS account is more like a TRANSIT account.

The money rarely stayed at one place.

It moved around.

And it seldom remained in the account.

How many of you are like that?

Man… The feeling was bitter.

Every 13th of the month, at 12am, my salary would be credited.

By 11pm, the same day, 3/4 of my salary was gone to pay bills.

I told myself back then.

“I want to be a MONEY MAGNET!

Not a MONEY REPELLENT!”

So what did I do?

I read books.

I found mentors. (Paid lots of $$$ to learn from them)

I followed proven systems that many successful people had followed.

You know some of those concepts.

Concepts like,

‘Save First and then Spend’,

‘Forced Savings’

‘Identify and Differentiate Between Your Needs and Your Wants’,

‘Invest in Equities, Bonds, Commodities, REITS, Properties, ETFs’

‘Robert Kiyosaki ESBI’ model

”

Coupled with my 3 year knowledge Diploma In Accountancy from Ngee Ann Polytechnic, I began to develop the right mix.

The right recipe. The right formulas.

It’s a bit like cooking Sambal Udang.

(picture from resepinannie.blogspot.com)

.

.

You need to find the right balance.

The right amount of cili kering (dried chillies).

Tamarind.

Salt. Sugar. Prawns.

Everything in the right proportion.

And….

My small, little advice.

If you have found a recipe and a system that works well for you…

Don’t have ‘itchy fingers’.

Stick with it. Follow the system closely.

Repeat the process again. Again. And all over again.

Till you reach your retirement objective.

It is that simple.

Simple yet sometimes, difficult to follow.

………………………………………

………………………..

……………..

Yes. If you have been trying to save money, and failed numerous times.

Let me tell you 1 thing.

It is not your fault.

We are human beings. We have our own DNA.

We have our strengths. And we have our limitations.

So the key here is for you to personalise your plan.

This is HOW I PERSONALISED my retirement plan.

As a Muslim, I know that Allah S.W.T. determines my rezeki.

Everything that I do, can only happen with Allah’s will.

……………………

……………….

……

Say: “Nothing shall ever happen to us except what Allah has ordained for us. He is our Mawla (protector).” And in Allah let the believers put their trust.)

Quran (Surah Tawba, Verse 51)

………………….

………..

….

Thus I made a decision, that whatever financial strategy that I am going to do.

I am going to do it the shariah compliant way. The Halal way in Singapore.

Because at the end of the day, its not all about strategies. Its about baraqah.

Its about seeking redha from Allah S.W.T.

I made up my mind.

I made a commitment.

I set myself to pursue knowledge to COMBINE the best financial planning practices in the conventional world and the Islamic Finance world.

I remember the story of “Rabbit and Tortoise”, that my teacher shared with me when I was in primary school.

You know the OVERCONFIDENT rabbit that lost the race to the tortoise.

The overconfident rabbit slept halfway, thinking he was fast.

He was quick. He was agile.

The slow tortoise will lose to him.

But lo and behold, the slow tortoise won the race because the slow tortoise was CONSISTENT.

…………………………………

……………..

What I learnt from this story is that you can be the best financial wizard in the world.

You can have the best retirement strategies in place.

Yet, if you are not CONSISTENT in applying them.

Having enough money for your retirement will remain a far-fetched dream.

………………………..

………………………….

I realise that a lot of people, treat money-saving habits like “hangat hangat tahi ayam.”

At first they get excited with the idea of retirement planning. But when they realize that it requires work, they feel let down.

Every other day, I have strangers asking my opinions on the latest get rich quick schemes.

Some asked for my opinion. Some asked for my endorsement.

(Something like this)

………………….

……….

….

I disappointed them by telling them in the face that there is no elevator to success.

You have to climb up the stairs.

I am a firm believer of ” Man jadda wajada, wa man zara’a hasada, wa man yajtahid yanjah ” Man jadda wajada, Siapa berusaha, dia dapat.

Man zara’a hasada means “sesiapa yang bercucuk tanam (Inshallah) akan menuai hasilnya.”

Man yajtahid yanjah means “sesiapa yang berusaha (Inshallah) akan beroleh kejayaan.”

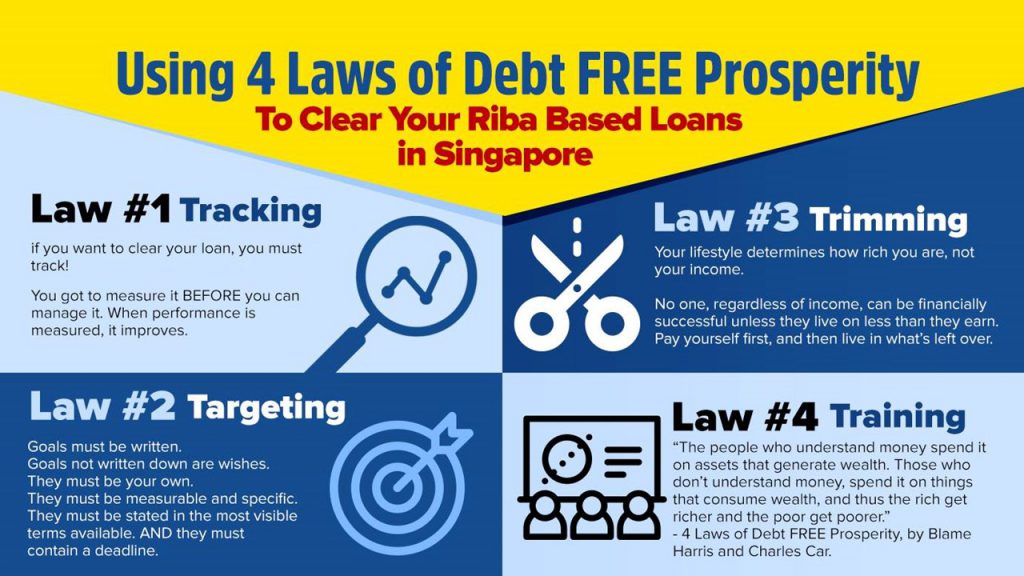

and when it comes to savings for retirement. You have to CONSISTENTLY set aside a monthly amount for your retirement. Don’t touch that money. Don’t stop.

Because once you stop, you lose your momentum. And it will be difficult for you to start again.

……………………………………………..

………………………………

………..

Rule #4. Be Flexible. Adjust

Along the way, we may face challenges.

Things don’t go as planned.

I always share with my clients. You draw a straight line on a piece of paper.

It may look straight in your eyes.

But how confident are you that, the straight line that you draw is really straight?

…………………………………..

……………………….

In life, you need to be flexible.

I love this quote by Confucius.

Adjust the action steps.

Work with practitioners.

People who hustle and make things happen on the ground.

They devote their entire life perfecting their craft.

Be humble. Seek help from these people.

These people know the tricks of the trade.

And most importantly, they do it the legal way.

In short, we call them street smart.

If someone is doing better than you, its because they know something you don’t.

Be flexible. Model a proven winner. Copy someone who is making a mint right now.

If things don’t work for you, don’t shift your goals. Adjust.

…………………………………….

……………………

……………

Rule #5. Don’t Give Up

We are lucky to be Muslims.

Because as Muslims, we believe in Allah S.W.T.

Whenever we face problems and challenges. Don’t place everything on our shoulders.

Remember what Allah S.W.T says

Innamalyusriyurah…

Setiap kesusahan, pasti ada kesenangan.

(Behind every difficulty is a blessing.)

………………..

As Muslims, our 6th pillars of Iman is Qada and Qadar.

My mentor always reminds me of Qada and Qadar.

Qada is ketentuan from Allah S.W.T.

Sunatullah that Allah S.W.T. has set.

Example, for rainy days, one of the signs is that the sky turns dark. Cloudy.

And rain falls from the sky. Not from the surface of the earth.

If rain falls, we cannot stop that.

However, we can AVOID ourselves from GETTING WET. HOW?

.

By opening an umbrella. Open and walk under that umbrella!

That Umbrella is Qadar. Which is our effort.

We cannot stop the rain (Qada) yet we can avoid getting wet by using an umbrella (Qadar).

Don’ be disheartened when you stumble and fall down while working towards your financial objectives.

Dust yourself up, stand and continue working towards your goals.

……………………………………………..

……………………..

Now… I hope you have benefited from my sharing on 5 Most Important Rules To Halal Savings For Your Retirement in Singapore.

If you are seeking a mentor, coach, consultant to share with you practical aspects on how you can protect your wealth using Halal Insurance in Singapore

OR

save, accumulate and grow your money the shariah compliant way in Singapore, I am always ready to help you.

I just came back from my holiday trip to Europe a week back, and I received a lot of emails, whatsapp messages, asking me specifically on retirement planning in Singapore. I am still following up, one by one. 🙂

……………………………………….

Since the Rebecca Lim’s fiasco, many of you have asked me on how to calculate how much you need to save today, so that you have enough money to retire comfortably in Singapore, and the best part, how to do it in the shariah compliant way. 🙂

(My mum and dad approaching their retirement years, relaxing at Table Mountain, in South Africa)

………………………………………………………..

……………………………..

……………..

I always share with my clients that how much you need to save today, is dependent on the type of retirement lifestyle that you want to lead when you choose to retire.

You choose whether you want to lead a sedentary lifestyle or a lavish one when you retire, or simply maintain your existing lifestyle.

Many of you, if you have been spending, example, $3000/mth today, you would not want to drastically reduce your spending power to $1000/mth when you retire right? Simply because you are not working and there is no cashflow coming in as before. 🙂

You will want to MAINTAIN your lifestyle.

……………………………………………………………………………….

…………………………………….

Today, I am going to share with you a very simple yet powerful retirement planning concept.

Let say you are 30 years old now. You would like to retire at the age of 60. Mortality age for average Singaporeans is about 90 years old. (Of course, there are people who lives much longer, but we take the age of 90 for this example.)

The period from 30 to 60 years of age is what we call the Accumulation Period.

Whereas from 60 years old to 90, is what we call the Retirement Period.

My question to you is this: When you retire, how much do you want to spend every single month?

If you ignore inflation, and you ignore investment return on your savings, how much exactly do you want to spend every single month?

$3000/mth? $5000/mth? $10,000/mth?

Write Your Answer On A Piece Of Paper: I want to spend $________ every single month when I retire.

Now take a look. Your ACCUMULATION PERIOD is 30 years and your RETIREMENT PERIOD is also 30 years.

Ignoring inflation and investment return, if you want to spend example, $3000/mth, when you retire, you have to also save $3000/mth today, for you to retire.

Right? 🙂

How much you need to save today, is dependent on the type of retirement lifestyle that you want to lead when you choose to retire.

You choose whether you want to lead a sedentary lifestyle or a lavish one when you retire, or simply maintain your existing lifestyle.

……………………………………………………………………………

…………………………………………..

When I share this concept with my clients, most are astounded. It is a very simple, but profound concept that you can use to calculate, how much you need to save now, every month to have the DESIRED retirement lifestyle you can have in the future.

Of course. After you know roughly, how much to save, the next question is how to grow that money, the shariah compliant way in Singapore.

Many of my clients understand that I build a long term advisor-client relationship with them to help them grow their investable assets (go download and read my book, if you don’t know what is investable assets) and at the same time grow their networth the shariah compliant way in Singapore.

……………………………………………………………………………

…………………………………………….

……………

In Singapore, there are a few ways to grow your investable assets, the shariah compliant way.

Firstly, buy shariah compliant stocks, direct from the market. (recommended only if you have the financial knowledge)

For me, this is a good long term strategy to include shariah compliant stocks in your portfolio to grow your money for your retirement.

Have a watchlist of shariah compliant stocks, and start doing your homework.

Download the companies’ annual report. Know how the company makes money. Calculate their profitability, gearing and investment ratios. Analyse deeply the trends, if the gross profit margin, the net profit has increased consistently for the past 10 years.

If the sales has increased, gross profit has increased, net profit has increased over the years, go through the company’s cashflow statement, to check that the company do not just have credit sales (close sales but customers owe them money in credit) , but can also are able collect money (cold, hard cash) from their sales.

There are many fundamental analysis that you should do when analysing and choosing shariah compliant stocks. The above is just 1 example. Learn about them first, before investing your money direct to the stock market. This is important because you would not want yourself to involve with maysir (speculation), when your niat (intention) is already to grow your money the shariah compliant way.

………………………………..

……………. Secondly, buy commodities like physical gold bar.

I see this more of a wealth preservation strategy. In your effort to accumulate your wealth, it is good to diversify and commodities like gold.

However, make sure that you buy gold bar, you can sell immediately to the seller if you urgently need money.

By the way, I wrote a 4000 words report on investing in gold. If you are my existing clients, and you are interested to learn more, you can request it from me (and get advice when you meet me for financial review). 🙂

……………………………….

……………..

Third strategy, which is my favourite strategy is investing your money in shariah compliant funds. This is my favourite strategy because I can do it passively.

I will skip my explanation on what is the difference between shariah compliant fund and conventional ones. What is riba, maysir, gharar. Imam Nawawi Riba rulings etc2…. (If you are interested to learn more, just fix an appointment with me, and I will share more)

…………………………………

…………………….

In this blog post, I will share why investing in equity funds are different that investing in stocks. I will speak in the perspective of making money ONLY. Usually, when my clients plan for their retirement, they will have a long investment time horizon. Perhaps 15-25 years.

The thing about investing in stocks, specifically penny stocks (small caps stocks), the stock price can go up and can go down, and can even go bust.

A professional manage shariah compliant fund works differently. The fund price can go up and it can go down, however, long term wise, it will always go up. Why?

Firstly, inflation. Example, you love drinking coffee. You drink it everyday.

(An “atas” coffee, I made for myself… )

……………………………………………………………………………..

……………………………………..

How much did you pay for your coffee? $1?

Another 10 more years, will your coffee still cost you $1?

Definitely NO, because the price will have increase because of inflation. Similarly, because the price of the coffee increase, when you check the trading, profit and loss statement of the coffee company, the sales will increase, the gross profit will increase, the net profit will increase, everything in the financial statement will increase, thus the stock price and in effect the fund price will also collectively increase.

…………………………………………………..

2nd reason, human population growth. Now, maybe in Asia Pacific, I assume, 10 million people drink coffee everyday. Another 10 years, will the figure remain the same?

Definitely NO.

Due to human population growth, more people will drink coffee. Similarly, because more people drink coffee, when you check the trading, profit and loss statement of the coffee company, the sales will increase, the gross profit will increase, the net profit will increase, everything in the financial statement will increase, thus the stock price and in effect the fund price will also collectively increase.

…………………………………

………..

3rd reason, you have professionals to manage your fund. There is a set of rules (qualitative and quantitative) for fund managers have to follow when selecting stocks specifically when it comes to shariah compliant fund.

One of the examples, if that the gearing ratio cannot be above 30%. Thus diligence is exercised when the fund managers select shariah compliant stocks in the shariah compliant equity fund.

If the stocks does not meet the criterias, and at the same time, are not performing well, it will be removed by the fund manager and replace by a better performing one. That is why shariah compliant fund price, specifically, can go up and down. However, long term wise, it will always go up.

……………………………..

………………..

……….

4thly, specifically for my clients, you have me to rely on, giving you advice when to do a top up, when the fund price is selling cheap. Example, you buy apples today. Price of an apple cost you $1. One day, it drops to $0.99.

$0.95.

And $0.90. What will you do? Just ignore it. You dollar cost average.

However, when the apple price goes down to $0.70, $0.60, financial advisors like me, will ask you to buy more apples, so that when the price goes up back to $0.90, $0.99 or even $1.10, you make more money. You enhance your portfolio returns by so much more. 🙂

………………………………………………………………………..

…………………………………………….

Alright….. I hope you benefit from my sharing. This is a recording of a video (which I recorded 6 years ago) , of a simple way on how to gauge how much money you need to save so that you can retire comfortably in the future.. A simple yet powerful strategy on retirement planning. Watch it now!

P.S. : If you find my sharing beneficial, do share this blog post with your love ones. Insya’Allah… 🙂

P.P.S. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

I was having a discussion with my colleagues, if there is demand for financial consultants, since consumers can just buy direct from insurance companies beginning next year.

In my honest opinion, there will still be demand for personalised service for professional financial consultants in the near future.

Let me give you a few real life examples, of why you will still need your financial consultant to plan, advice and service you.

1) Tried To Claim Outpatient Hospital Bills Unsuccessfully

I was referred to an engineer late last year. He was hospitalised.

He understands that, he can claim pre and post hospital bills up to 90 days.

With confidence beaming from his face, he dropped by the insurer’s office to meet the claim officer.

Submitted the bills and the claim officer rejected him outright, stating that outpatient treatment could not be claimed.

He was confused of his predicament. He met me. He narrate and pour out his story to me. I listen. I then explain to him that he needs to EXPLICITLY state that the outpatient treatment bills that he is submitting are for post hospitalisation bills.

Post hospitalisations bills can claim up to 90 days, and Alhamdulillah, I claimed for him successfully. 🙂

2) Stroke Patient’s Family Don’t Know He Has A Severe Disability Insurance Plan

This was another referral. I come down to his house. I met his son. After chit chatting for a good 20 minutes, I begin to realise the purpose of my visit.

I told him, ” Actually, I come down to your house not to meet you, but to meet your father. I was referred to meet your father. Where is your father?”

He replied me, ” My father is in the room.”

I told him, “Asked him out lah.”

He replied me, ” My father is sick. He got stroke…”

I looked at him empathically, concerned and asked him in a deep, lower tone of voice….“Ok… Insurance all claimed already lah?”

He looked at me with despair and told me, ” My father terminated all his insurance policies already. He has none left…”

I then asked him, “How about Eldershield plan?”

He looked at me with a blur look and replied, “Terminate also.”

I asked him affirmatively, “Confirm???”

He shrugged. I get him to write his father’s name and IC number on a piece of paper, and I personally called the insurer.

Lo and Behold, his father has an in forced severe disability insurance plan known as Eldershield!

His father suffered from stroke for 3 months already, and never claim from his Eldershield plan. I then guide his son, on procedures to help his father claim from his Eldershield plan.

If he was not referred to a qualified financial consultant, there might be a glaring possibility, that this very client will never claim his insurance at all.

……………………………………………………………………………………………………………………….

3) Confident Got $300,000 Death Coverage

I get to know this client from the outreach financial planning workshop, we did at one of the community centres in Singapore.

I came down to his house and he signed up hospital insurance plans for himself and his family.

Subsequently, I asked, if he dies, how much his wife and 2 kids will get?

He answered me confidently, “No worry Helmi. If I die, my family will get $300,000.”

I said, very good. He has done his planning very well. His disposable income is $2500 per month, $300,000 is 10 X his Annual Salary, which as a rule of thumb means he is sufficiently covered!

Nevertheless, I asked for his policy document.

He rummaged through the drawer in his room and handed it over to me. Flipping thorough the policy document, I realised that he has an investment linked policy.

That investment linked policy comes with a “rider”. That rider states that if he dies DUE TO ACCIDENT, his family will get $300,000.

HOWEVER, if he dies a normal death, his family will only get $30,000. Imagine the shock on his face, when I told him this. He has been telling his wife, over the years, that if he dies, his family will get $300,000.

These are just a few examples, why financial consultants are still needed in Singapore.

Singaporeans are generally busy people, and require the help of establish financial consultants like us, to educate, advice, assist, partner and motivate them to achieve their financial goals, to the best of their ability. 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

You may find me a very FAMILIAR face in Toa Payoh MRT, in East Point, in front of Civic Centre…. everywhere….all over Singapore. 🙂

…and in meeting Singaporeans…Yes! real people like you and me….I discover something disturbing…

Many people failed to plan for their retirement….and here are their excuses comments.

1) “My money in my CPF is already a lot, enough to fund for my retirement needs”.

My reply: Most of your money in CPF has been used to pay for your house. You need to start saving now.

2) “My retirement days still FAR AWAY. I need to use my money now to buy CAR, HOUSE….. I will do it when I am older”

My reply:The opportunity cost of procrastination is huge. You can start something small, and gradually increase it. You need to start saving now

3) ” How do I plan for my retirement? No one has helped me before in this.”

My reply:Call Helmi Hakim at +65 96520134. He will help you plan for your retirement.You need to start saving now.

4) “I got too much financial commitments. Need to take care of my parents, children, pay off mortgage loans etc”

My reply:Create your own personal cashflow statement and try to reduce your variable outflow. You need to start saving now.

5) “When I retire, I will downgrade my house to a less expensive one and the profit, I will use it for my retirement”.

My reply: This method may inject uncertainty into the process because the property market can be volatile and if you were to retire at a time when the value of your real property crashes, your main source of retirement nest egg would be SEVERELY AFFECTED.

Furthermore, a decision to downgrade may not be an easy one to make on an emotional and psychological level as you may be so used to a certain standard of living that you will find it difficult to downgrade when the time comes for you to do so.

Therefore you need to start saving now.

…………………………

AHA…Now, we have been talking about retirement planning. Have you start planning for your retirement? 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

A certified financial consultant, Helmi Hakim has won praise for his patience, perseverance and practicality when solving his clients’ financial concerns. For more information on how you can manage your finances better, contact Helmi Hakim at 96520134.