We are in the 2nd week of “circuit breaker” in Singapore.

Although I have to work from home, I’m blessed because I still have a job that makes me excited everyday. 🙂

Alhamdulillah…I am thankful to NTUC Income for acknowledging and recognising my hard work by having my name mentioned in Straits Times.

I would like to thank my wife, Shikah Anuar for being my pillar of strength and believing in what I do.

My manager, Irene Ho for your continuous guidance to keep me focused on my goals.

I would like to thank my clients for your trust and support over the years in engaging my expertise to help you plan your finances, the shariah compliant way in Singapore.🙂

There are a lot of ups and downs. Moments where I just feel like giving up. Yet your tremendous support and encouragement continue to spur me forward.

Thank you all once again! 🙂

……………………

……..

….

Many have asked me on the story of my “overnight success”.

Being an Islamic Finance practitioner in Singapore since year 2007 is a dream come true for me.

It is my 1st job after ORD from the army.

Yet, my story began long before that.

…………..

……..

… My ambition when I was young was to become a school teacher. I love interacting with kids. And I love teaching, sharing my knowledge with others.

So after my O’Levels, I applied for Diploma in Teaching of Malay Language with Ministry Of Education.

I was called for an interview but unfortunately did not make the cut.

I was doing OKAY with my Malay language but I think my “peribahasa terabur” at that point of time because I was too nervous! That was my 1st interview in my entire life!:p

………………..

……

………

So my second option, was to go for my Diploma in Accountancy.

My logic back then is that every company in Singapore needs an accountant.

To my mind at that point of time is that an accounting job is the most sheltered and safest job one can have.

The job will be irreplaceable and very secure!

So I applied for NP. I was living with my parents at Marsiling.

(My family and I celebrating Hari Raya a few years ago)

(Beautiful and spacious Marsiling before the BTO flats sprung up like mushrooms over the years)

.

.

.

I thought studying in Nanyang Polytechnic – which is just next to the MRT – would be very convenient.

When I got the results of my posting., I got the shock of my life. I found out that NP stands for Ngee Ann Polytechnic!

and not Nanyang Polytechnic!

………………………………….

…………………………

……………

There is hikmah to be rejected for my interview to be trained as a school teacher

and hikmah for me to accidentally choose to study in Ngee Ann Polytechnic,

because that choice CHANGED the course of my entire life!

In Ngee Ann Polytechnic was where I was exposed and trained to love and understand numbers.

Not numbers without meaning. 🙁 Practical numbers that will determine the life of a business. 🙂

Will the business succeed? 🙂 Or the business fail? 🙁

Can the stock make money? 🙂 Or the stock lose money? 🙁

We learnt how to create company’s annual report.

Trading, Profit and Loss Statement

Balance Sheet.

Statement in Changes of Equities

ALL FROM SCRATCH!

We computed Financial Ratios.

Analysed them. Interpreted them.

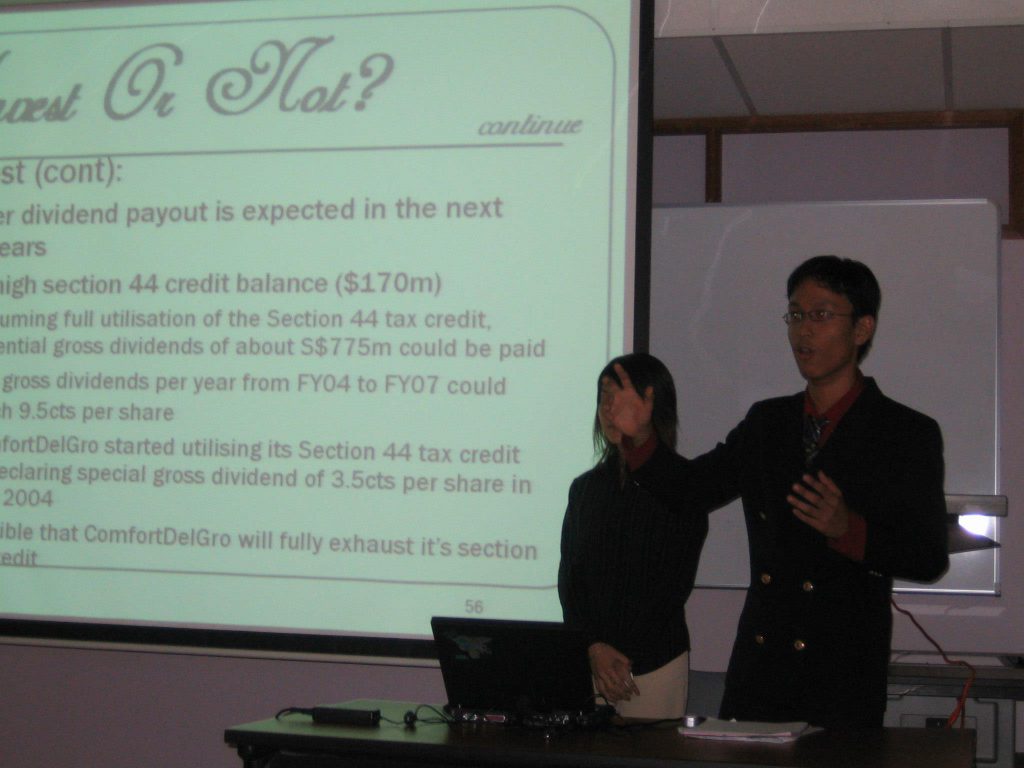

And presented them in front of our “clients’. Alhamdulillah. That was my first exposure to public speaking

and someway, somewhat, somehow, I enjoyed it…. 🙂

(My first experience presenting details of a financial statement in front of our “clients” 15 years ago)

……….

……….

………….

And in Ngee Ann Polytechnic, I joined the business club.

Me and my business partner were 18 years old at that point of time.

We went for a business plan competition and Alhamdulillah was awarded with a funding of $3000. (that was a lot of money when you were students)

As we were below the legal age to set up a company, we used our fathers’ names to register a private limited.

The business failed.

Yet I learnt many important lessons from that episode that shapes me to who I am today! 🙂

(My business while I was still studying in Ngee Ann Polytechnic)

(While waiting for my enlistment in the army, I did a sales job promoting credit cards for a marketing company.

Alhamdulillah. I topped the whole company for 3 months before my enlistment.)

…….

(Myself in the middle after POP from BMT)

.

.

Whilst serving my national service, i did my research.

I knew back then after ORD,

I wanted a job that allows me to have freedom of time.

I don’t want a desk bound job. I want to be my own boss.

I don’t want to stick myself to the 8-5 routine (just thinking about the morning peak rush hour makes my head spin)

And at the same time allows me to share my knowledge on finance with the common people on the streets.

That is where a career as a financial consultant looks appealing to me.

I did my research.

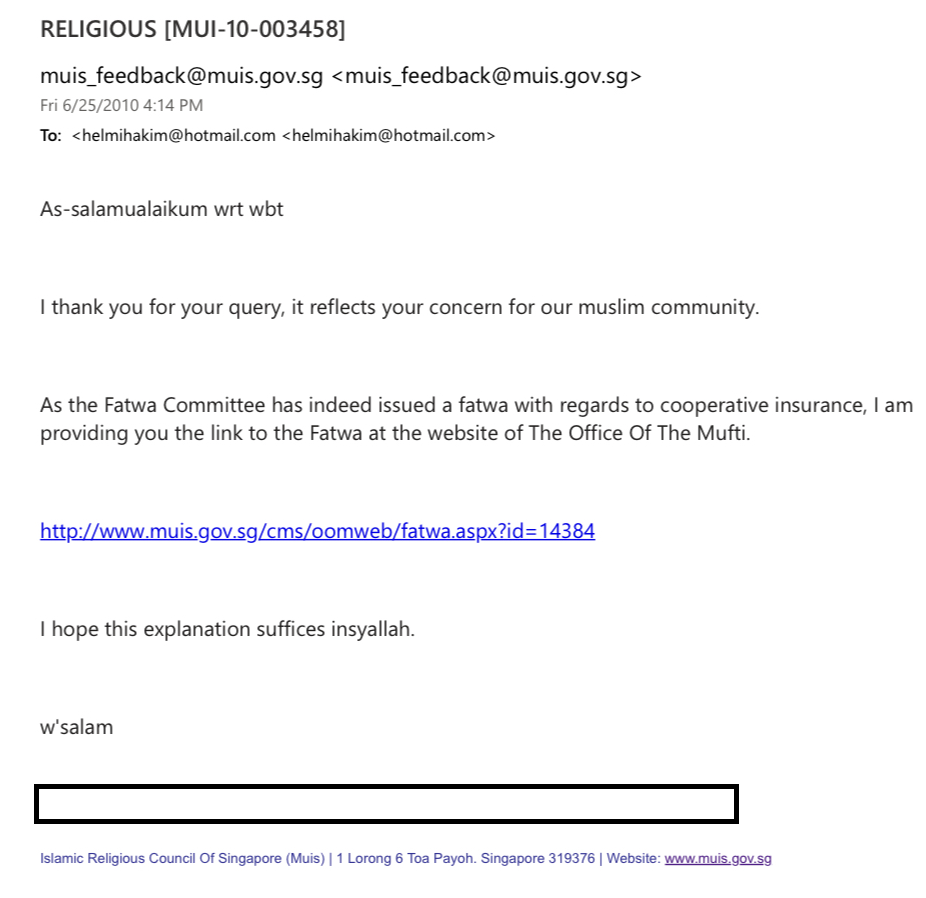

1 thing that I want to be assured is that my job must be Halal. I emailed MUIS and was directed to the fatwa on permissibility of cooperative insurance in Singapore.

.

.

.

Alhamdulillah. We know the Hukum of getting cooperative insurance in Singapore is Harus (neutral).

.

.

Yet, I know financial planning is beyond insurance.

What about savings for child’s education? Retirement? Wealth Accumulation?

And I discovered NTUC Income has numerous shariah compliant funds at that point of time.

NTUC Takaful fund (which now follows the Dow Jones Shariah compliant screening methodology)

NTUC Amanah Equity fund

NTUC Amanah Bond (Sukuk) fund

To me, having shariah compliant funds closely monitored by Islamic Finance scholars 24/7 is important.

Thus, that’s where I began my journey as an Islamic financial consultant in a cooperative insurer in Singapore.

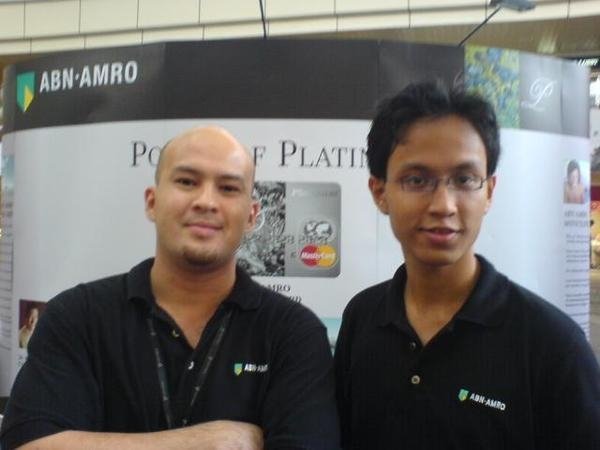

(Picture with Alvin Soong’s team, my 1st mentor who brought me in to the financial planning industry a decade ago)

……………………

……….

………..

When you first start out in the financial planning industry.

It was not easy. It was not a bed of roses.

If you think just by joining the financial planning industry, can immediately drive flashy cars.

Buy a yatch. Relax by the beach everyday.

No. Its far from it.

Many times, I felt like giving up.

In fact, I felt like giving up everyday.

To me giving up is easier than persevering.

………………………….

…………………….

..

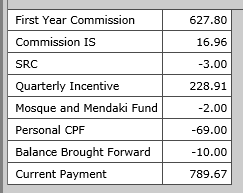

When we first started, we earned based on commissions.

(My first month commission when I first started my career as a financial consultant in year 2007)

.

.

.

We don’t have the luxury of immediately earning a stable basic salary $2-$3k/month.

.

.

Not only that. We have costs to pay.

If you see financial consultants doing roadshows at Malls or exhibitions, on average they need to pay $300/person for rental of space.

So imagine. My $700 commission minus off $300. I am only left with $400 to survive.

.

Not only that. Year 2008, 2009.

Was the subprime mortgage crisis which lead to the global economic crisis.

That was the period of Lehman Brothers Minibonds Saga.

Many people were reluctant to part away with their money. People were very afraid of financial consultants.

I remember doing roadshows, and was told “Young man. I just lost $100,000 in XXX scheme. And you want me to invest with you?”

.

. It was a difficult phase of my life.

I remember at that point of time……

Not even having enough money to top up my EZ Link card because minimum top up is $10. I only had $5 in my wallet.

I remember at that point of time,

having to turn down invitations by friends to eat buffet for lunch at the restaurant because I didn’t have enough money.

I remember at that point of time,

the nikmat of sharing briyani on a dulang at Wak Tanjong mosque when I broke my fast during the month of Ramadan.

That briyani was a luxury to me because I only had single digit $ in my bank.

…………………………

…………………

………….

These memories evoke deep sad bitter sweet emotions within me that I can feel even till now.

I felt like a total failure.

But as Muslims, I always remember this. We are not alone. We have Allah S.W.T.

I make a lot of doa to Allah S.W.T.

As Muslims, I remember the words of Allah S.W.T.

…………………………………

………………..

…………

Alhamdulillah. Allah’s promise is true.

With strong support from my family and clients, I persevered. (eternally grateful for them because I have nothing to showcase at that time.)

After hustling for a while, things got better.

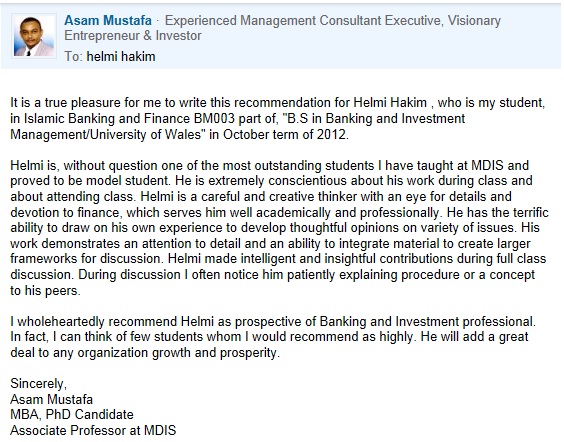

Once things stabilised, I then subsequently upgraded myself by taking my degree, Bachelor of Science (Hons) Banking and Wealth Management with University of Wales (UK).

My favourite module back then was Islamic Banking and Finance.

Alhamdulillah, with the guidance of our beloved teacher , Professor Asam, I aced the module.

.

(Testimonial from Islamic Finance Professor during my undergraduate days)

.

.

And Alhamdulillah, what came as a surprise for me at that point of time was when I was informed that I was amongst the top 3 students in my whole cohort upon my graduation.

.

.

You have to understand this.

All my classmates were financial consultants, bankers and seasoned practitioners (some with decades of experience).

And to become amongst the top 3 students never came across my mind.

.

.

(My proud moment receiving an award on stage)

.

.

.

That gives me the determination and direction..

Allah gives me the rezeki.

The amanah.

Puts me in a very favourable position. For a REASON. (if you know me on a personal level, I rasa betul2 tak layak. There are many others who are way better than me)

I find that this is part of fardu kifayah.

And I have the responsibility to shoulder this tanggungjawab to share with our community the pragmatic aspects of Islamic Financial Planning in Singapore.

I have to prove and make it work in Singapore.

For me success in Islamic Finance is not just me, myself clearing my own riba based loans and growing my own money the shariah compliant way in Singapore. Success in Islamic Finance is helping others plan their finance, without riba, maysir and gharar in Singapore.

Why I continue to stay in this line after so many years is

because I believe I will be able to HELP many more Muslim families plan their finance,

the shariah compliant way in Singapore.

After I die, in the hereafter, at yaumul mashar, I need to present my deeds in front of Allah S.W.T.

I want to be certain.

Ya Allah. On this earth, you bless me with the rezeki to learn about Islamic Finance.

and I, Helmi Hakim had done my utmost best to educate and share with as many people on how they can plan their finance, the shariah compliant way in Singapore.

My mouth.My hand.My legs.My head.My heart.

All as one will testify that I have done my utmost best, to educate and share with as many people on how they can plan their finance, the shariah compliant way in Singapore.

And all, be it you are my clients. Or just anyone who has benefited from my sharing.

You will be my witness.

You will be my lawyers on judgement day, that Islamic Financial Consultant, Helmi Hakim when he was on earth, he had done his utmost best, to educate and share with as many people on how they can plan their finance, the shariah compliant way in Singapore.

Please send him to Jannah. Ya Allah. Amin. Amin…. Insya’Allah. 🙂

…………………..

……………..

………….

Now… I hope you have benefited from my sharing on the Story of Islamic Financial Consultant, Helmi Hakim.

If you are seeking a mentor, coach, consultant to share with you practical aspects on how you can plan your finance, the shariah compliant way in Singapore, I am always ready to help you.

Many of you might have known me as the financial consultant who specialises in helping Muslim families plan their finance, the shariah compliant way in Singapore.

(Myself sharing on Islamic Finance in Singapore on a national TV show, “Alah Abang, Amboi Kakak”)

.

.

In my profession, I met skeptics who have misconceptions about shariah compliant financial instruments in Singapore.

And I am here to provide enlightenment. Insya’Allah. 🙂

………………………

……………….

………

Misconception #1: Shariah Compliant Financial Instrument is EXPENSIVE

.

FACTS:

All plans from financial institutions come with charges.

The shariah compliant ones. Or the non shariah compliant ones.

How to know there are charges?

Simple.

Get a plan today, and terminate it 6 months later. Your cash value will be 0 or lesser than the amount you put in because of the upfront charges.

Let’s face it.

Nothing in this world is free.

Yet, if you were to calculate the effective profit rate (Malays call it untung bersih) of shariah compliant investment over a time period of 20 years.

The effective profit rate is WAY BETTER than effective interest rate of most conventional financial instruments out there.

You fulfill your long term financial objectives, the shariah compliant way in Singapore.

You get the best of both worlds. Dunya.

And akhirah. Alhamdulillah. 🙂

(Islamic Finance practitioners constantly upgrading ourselves, learning new market updates conducted by Brother Adnan from Wellington Management, NTUC Takaful Fund manager.

Wellington Management has been managing NTUC Takaful fund since 17 Oct 2010)

………………………..

…………

….

Misconception #2: Shariah compliant instruments are actually not Halal

.

The 2nd misconception I get is that Shariah compliant instruments actually not Halal.

FACTS:

The basic rulings of Muamalat.

……………..

………..

“All things are considered lawful, except for what has been prohibited”.

……………….

………..

………..

We know riba, maysir (gambling, speculation) and gharar are PROHIBITED.

You can’t invest in Haram businesses involving pork, casinos, alcohol and weaponry.

And there is a set of financial ratios shariah compliant investors have to observe.

………………………………..

…………………..

………….. One of my favourite questions.

Today, you are an INVESTOR.

You open up a brokerage account. And you want to invest in stocks.

Of course lah, you want to invest in Halal stocks. Not Haram stocks.

How to know the stock is Halal or not Halal?

In the world, there is this thing called shariah compliant screening methodology.

(One of the platforms I am using now to screen for shariah compliant stocks)

Dow Jones Shariah compliant screening methodology

MSCI

AAOFI (those in gulf countries like Dubai, Bahrain, Kuwait, Oman, Saudi adopted this)

Al-Rajhi

KSE Meezan

Malaysia also has their shariah screening methodology by Bank Negara.

Each screening methodology has their panel of Islamic Finance scholars to ijtihad and determine the stocks Halal or not Halal.

…………………….

……………..

….

Why is it important to have panel of Islamic Finance scholars?

Because what is Halal now might not be Halal 1 year, 6 months or even 3 months later.

~~The portfolio of shariah compliant stocks changes over time.

……………………….

…………………

……….

The duty of the Islamic Finance scholars is to monitor if the stock is Halal or not Halal.

REAL TIME.

In accordance to the shariah compliant screening methodology adopted.

This gives us investors the peace of mind that our portfolio is not just 60% shariah compliant.

Not 70% shariah compliant.

But 100% shariah compliant!

Alhamdulillah 🙂

…….

….

…

Misconception #3: Islamic Insurance is only for old people

.

Another misconception that I always got is that Islamic insurance in Singaporeis only for old people.

You know.

Atok atok.

Nenek Nenek.

Alaaaaahhhh… Basically the warga emas generation.

We are the Instagram generation! Still young.

Won’t fall sick easily one! Waste money only buy insurance when still young and energetic.

You know what?

I used to feel the same way too.

My perspective CHANGED when I stepped into the financial planning industry in the year 2007.

And it cemented further when I was hospitalised for 9 days due to high fever.

.

FACTS:

Young people. Old people. Teenagers.

Infants. ALL OF US NEED INSURANCE!

(Myself spending malam raya alone in the hospital. Sendu….)

To me….

Halal insurancerepresents hope.

It represents love.

It represents dignity.

It represents peace of mind.

It represents Aspirations. Dreams. Promise. Shelter.

.

.

(Alhamdulillah. Rezeki from Allah S.W.T.

Doctor allowed me to leave hospital for a few hours to celebrate Hari Raya with my family.)

…………………..

In your pursuit to achieve your goals in life, always….

Always… Remember this…

“Halal Insurance is a very, very important asset in your balance sheet.”

Be it you are old.

Young. Single. Married.

You need contingencies in a form of Halal Insurance.

It is like cruise ship. We know cruise won’t sink.

But why are there life boats in place? The life boat is JUST IN CASE. Halal Insurance is JUST IN CASE.

……..

….

…

Now… I hope you have benefited from my sharing on 3 Misconceptions Millennials Have About Shariah Compliant Financial Instruments In Singapore……

If you are seeking a mentor, coach, consultant to share with you practical aspects on how you can plan your finance, the shariah compliant way in Singapore, I am always ready to help you.

At times, when I discuss wealth management strategies with my friends, they say it’s difficult to make money the shariah compliant way in Singapore.

It’s easier in Malaysia.

In Indonesia. In Bangladesh. Or in Saudi Arabia.

But not in Singapore.

As a Muslim financial consultant who specialises in helping Muslim families plan their finances the shariah compliant way in Singapore, I am here to debunk such limiting beliefs.

I sum in up with my secret ABCDEFGH formula… I learnt it from my friends, fellow financial practitioners, and then innovate it further to ensure that it is customised and suitable for Muslims in Singapore.

With only the price of a plate of nasi lemak with crispy chicken wing ($5/day),

or $150/mth, you can kickstart your investment plan.

You can start planning your finance the shariah compliant way in Singapore.

Yes… With that $150/mth you can have access to shariah compliant stocks in our shariah compliant fund.

Shariah compliant stocks like….

Apple Inc

Microsoft Corp

Intel Corp

Google

Adobe

Harvey Norman

You DON’T have to fork out hundreds of thousands of dollars to buy shares.

Yes! At a price of a plate of nasi lemak with crispy chicken wings ($5/day)

OR only $150/mth,

you can begin to invest in shariah compliant fund that consists of these shariah compliant stocks. Super affordable right? 🙂

……………………………………..

…………………

..

Better Returns

You and I know that there is this thing called inflation.

It means that the value of your money erodes. Your purchasing power reduces.

Simply to say, your plate of nasi lemak with crispy chicken wings that costs you $5 today, will DOUBLE in price 10 years down the road.

The only logical choice that you have is to invest.

Make your money work harder.

Invest and grow your money to hedge and beat inflation.

And while you are at it, why don’t you do it the shariah compliant way?

Arrange “Your Financial M.A.P.” session at Takaful.sg for FREE.

And I will share with you more of my simple, easy to follow and proven financial strategies, that can help you get an effective PROFIT rate of between 3-5%/annum for an investment time horizon of 20 years.

That is better than leaving your money under your pillow or perhaps for some of you, in

your Khong Guan biscuit tin.

Do it with me.

And do it the shariah compliant way at Takaful.sg

……………………………………………….

…………………………………..

……………………

Coverage

Gone are the days, where when we mentioned coverage, we have to do it the conventional way.

Today you can have Death, Total & Permanent Disability AND Critical Illness coverage, the shariah compliant way.

You can adjust the coverage, that you want.

And the plan comes with a shariah compliant underlying fund.

In addition to that, an aqad contract can be done to remedy Maysir (Speculation) and Gharar (Uncertainty).

……………………………..

………………….

Diversification

With a limited amount of money, you can diversify your funds.

Yes… With that $150/mth you can have access to shariah compliant stocks in our shariah compliant fund.

Shariah compliant stocks like….

Apple Inc

Microsoft Corp

Intel Corp

Google

Adobe

Harvey Norman

You know the old saying, “don’t put your eggs in one basket”.

Again. Arrange “Your Financial M.A.P.” session at Takaful.sg for FREE.

And I will share with you my simple yet effective shariah compliant diversification formulae.

In addition, to the diversification strategies, I shared above.

It is customised specifically for Muslims who live in Singapore.

Schedule a session now! 🙂

………………………………….

……………..

……..

Easy Investment

A lot of my clients invest in stocks.

When I mention invest in stocks, I really mean it.

They do their homework.

They download the companies annual report.

And read the director’s statement.

To understand the companies direction better, they do a SWOT analysis on the companies.

Fundamental Analysis. Calculate the profitability, liquidity and investment ratios….

Vertical, horizontal analysis on the financial statements.

Calculate the intrinsic value of the particular stocks. Immerse themselves with further technical analysis.

100 days moving average, 150 days moving average. Many, many more time consuming researches…

………………………………………………..

………………………………….

In the end, I looked at them sympathetically and asked them… “Tired or not???”

Most replied with a look of despair on their face, “Of course tired lah!!”

And I probed them further, “Where do you find time to do all those time consuming research?”

Most replied when they came back home after 10 full hours of office work.

Go back home.

Straight to their computers.

Staring at the screen.

Busy punching numbers into their excel spreadsheets.

Stared hard again at the flickering charts on the screen.

Every. Single. Night. Vicious cycle. And it continues on and on.

I told the, why not choose the easy way?

Dollar Cost Average… Put money monthly every month, and top up when the market price goes down.

Still can make a good, fair share of Halal profits.

And, now imagine.

All the time, you save, from having to spend countless hours of research,

you begin to spend it on your wife and kids,

your love ones.

(Myself with my wife, enjoying ourselves during our honeymoon at Morocco)

That is why I love this formula.

Easy Investment = More Quality Time With Your Love Ones = Happier, Blissful and More Fulfilling Life

………………………………………….

……………………………..

………………..

Flexibility

You can choose to take premium holiday.

Meaning today you start with the shariah compliant investment plan.

In the future, if unfortunate circumstances, cause you to be financially tight, you can stop paying the premium for a while.

And resume back when you are financially OKAY.

You can also adjust your premium accordingly.

Now you start your shariah compliant investment plan @ $200/mth.

In the future, when your pay increases, you can always increase to $500/mth or vice versa.

Super flexible right? 🙂

………………………………

………………

…………

Great Support System

Let me share with you a little secret.

Almost half of my clients who engaged me for shariah compliant investments have finance training background.

They either have a Diploma or Degree in Accountancy/Finance.

Or professional certifications like ACCA etc2.

The reason why they choose investing with me, is because of Great Support System.

We leverage on the expertise of professional fund managers.

Remember the scenario I shared above.

Today, you screened a stock, and you deemed it shariah compliant.

Another 6 months down the road, the stock may no longer be shariah compliant.

Because shariah compliant is not just “No Pork, No Lard”.

There are certain financial ratios that we have to abide to.

Where can we find TIME to analyse it every single month?

Precisely. Leverage on the expertise of professional fund managers.

There is so much, I have to share on the beautiful part of Great Support System.

But I will not divulge it here in my blog. Because some of them are my trade secrets.

Trade secrets that differentiate me from the rest of the 20,000 financial consultants in Singapore.

Arrange “Your Financial M.A.P.” session at Takaful.sg for FREE.

And I will share with you how you can benefit personally when you engaged me as your financial consultant.

Your partner to help you grow your wealth, the shariah compliant way in Singapore.

Insya’Allah. 🙂

……………………………………..

……………………

…………….

Halal

There is really a lot of strategies for you to earn your money.

No point make money, when it’s not Halal. Your rezeki is everywhere.

In the subsequent blog post, Insya’Allah, I will share with you in greater detail on shariah screening methodologies that is currently used in the world.

For now, we stick with these simple, yet powerful formula.

So, next time, if anyone tell you that it’s difficult, to plan your finance the shariah compliant way…

Tell them this simple, yet powerful ABCDEFGH secret formula.

See you around soon. Jazakallah Khayran! 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

Some of my peers in the industry have been asking…

“Helmi… You always talk about Islamic Financial Planning. What exactly is Islamic Financial Planning? How is Islamic Financial Planning different than conventional planning?

Can we apply it exactly in Singapore?”

………………………………………………

…………………………………

………….

Yes. I specialise in helping Muslim families in Singapore, plan their finance in a shariah compliant way.

In accordance to theQuran (The Word of God)

And Sunnah (Traditions of Prophet Muhammad P.B.U.H).

One of the most important element of planning your finance the shariah compliant way is that you need to ensure that the financial strategies you advocate is free from prohibitive elements like riba, maysir and gharar.

AND the financial instruments that you choose is ALSO free from prohibitive elements like riba, maysir and gharar.

a. Riba, meaning payment or receipt of interests, is strictly forbidden.

Allah S.W.T said in the glorious Quran, Surah Al Baqarah, Verse 275:

“Allah has permitted trade and has forbidden interest”

………………..

………

.

b. Maysir, meaning any form of gambling. And Gharar, meaning uncertainty. Both are not allowed.

As stated in Surah Al-Maeda, Verse 90:

“O ye who believe! Intoxicants and gambling, (dedication of) stones, and (divination by) arrows, are an abomination,- of Satan’s handwork: eschew such (abomination), that ye may prosper.”

……………………………………

……………….

………

I like to give my clients, simple examples.

To explain difference between Riba (interest) and Profits.

This is important because many people out there get confused and thought that riba (interest) and profits are the same.

…………………..

………..

Example, today, I lend you $1000.

Tomorrow, I ask you, to pay me back $1001. That additional $1 is riba…

Even though, it is only a small amount of $1. That additional $1 is riba. Riba is not permissible in Islam! ……………………………………………………………….

………………………………………

Now, let me explain profit.

Example, today, I set up a drink stall.

I sell Bandung drink.

My cost per cup of Bandung drink is 40 cents. (You know the rose syrup, milk, water and ice)

I sell, the Bandung drink for $2. My profit is $1.60. Profit is permissible in Islam!

…………………………………………………………..

…………………………………………

………………….. Some people asked me, “Is it necessary, to plan my finance the shariah compliant way? I think, as long, I make money, its okay right? No need to be too concerned if its halal or its not.”

………….

…….

I told them, I am a trained financial consultant.

I can present you ideas on how you can grow your money the shariah compliant way and also the non shariah compliant way. Convincingly.

And if you can grow your money the shariah compliant way, why choose to do it the non shariah compliant way?

……………………………………………………………………………………………..

……………………………………………………………..

In addition to that, I told my clients and also my mentees. In our profession as a financial consultant, we are doing good jobs for our community.

(A picture of my family and myself)

You know, at times, I meet a family, and I bring about the idea of saving money for child’s education, to the sole breadwinner.

The Abang will look at me and say, “Child’s education? You mean you want my child to go to university? I myself, only have O’Level. How can you expect my child to go to university?”

………………………………..

…………………………………….

I told him, “Yes! Its possible! Your child will grow up and can go to university in the future!

He can be a lawyer, teacher, engineer, any profession that can help the community…He will be someone successful and beneficial to the community!!”

………………………………………..

…………………………………………….

AND we went one step further, we help that Abang plan for his child’s education, the shariah compliant way.

Not only that Abang helps his son, he also do it the blessful way. The shariah compliant way.

Both me, as his financial consultant, and him, as my client, will get passive pahala (good deeds) for the next 15-20 years of the plan. Its because both of us choose Islamic Financial Planning in Singapore.

We choose to do it the shariah compliant way. Avoid riba. Avoid maysir. Avoid Gharar.

That is what Islamic Financial Planning is all about.

Isn’t that a good position to be in? 🙂

…………………………………………………………………………..

……………………………………………….

So for those of you, who have been considering Islamic Financial Planning, take a look at the Financial Planning Building Blocks below and whatsapp/SMS me, Financial Consultant, Helmi Hakim at 96520134 to schedule an appointment. Insya’Allah! 🙂

(Financial Planning Building Blocks To Plan Your Finance With Financial Consultant, Helmi Hakim)

I travel a lot for my holidays and get quite worried reading the headlines of what is happening around the globe. Hence, I put forth some risk management strategies that I personally use when travelling overseas.

Segregate your money. Whenever I travel overseas, I segregate my money into 2 wallets.

Some of my money I left it in the safe at the hotel room. Some of my money I kept it in the hidden compartment in my bag. Most important of all, don’t put your money in one place. It is because if you lose them, you will be at your wit’s end.

.

.

.

2) Photocopy your passport, flight travel itineraries, hotel bookings.

I ensure that I photocopy my passport, flight travel itineraries and hotel bookings.

I also make a back up copy on my Iphone and Ipad, either by snapping a photo or having them in my Iannotate PDF app software. (Of course, my devices are secured with a pin password)

In addition to that, I have an additional copy stored in my google drive.

If I lose my passport or any important travel documents, I will have all the documentation ready, in place.

.

.

3) Have the Ministry Of Foreign Affairs Contact in your mobile phone

Alhamdulillah…. So far, I don’t need to seek assistance from Ministry of Foreign Affairs when I

travelled overseas for holidays.

However in my profession as a financial consultant, I remember assisting one of my friends claims,

when his close family member passed away overseas.

Have the Ministry of Foreign Affairs contact in Singapore at (65) 6379-8800 too, just in case.

Save it in your mobile phone now! 🙂

.

.

.

4) If you drive in to Malaysia, bring your steering wheel lock.

Yes. I bring my steering wheel lock when I drive in to Malaysia. I know, sometimes we take safety for granted.

As part of my risk management strategy, I use my steering wheel lock to secure my car after I park it.

In addition to that, remember not to park your car at secluded area. If you plan to dine at the restaurants nearby, ensure that your car is in plain sight of your view at all times.

.

.

5) Buy travel insurance

If there is a flight delays, flight is being cancelled, loss of baggage or due whatever reasons, you know that you will have a back up plan in place.

When you go for holidays, you want to let down your hair and have a peace of mind. Buying travel insurance is essential and necessary as part of your risk management strategies when travelling overseas.

.

.

:: Bonus Tips ::

– Read Tripadvisor Reviews of the place you want to go to. Its because some places there are a lot of pickpockets.

– If you went to Europe, intend to buy branded, high end items, bring an additional bag. Shopping bags from designer labels stores attract attention from undesired individuals.

…………………………………………………………

……………………………………………………….

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then please click here…

A certified financial consultant, Helmi Hakim has won praise for his patience, perseverance and practicality when solving his clients’ financial concerns. For more information on how you can manage your finances better, contact Helmi Hakim at 96520134.