“Helmi Hakim. I want to buy a house in Singapore. I dont have money to pay full in cash thus I have to take a loan.

Is there shariah compliant home financing facility in Singapore?”

………………………………..

………………

……….

I have made it clear that there is NO shariah compliant home financing facility in Singapore at this point of time.

That’s why I created Takaful.sg with my unique Your Financial M.A.P. Model™ to share simple yet powerful strategies on how you can clear your Riba Based loans in Singapore.

In this blog post, I am going to share with you how shariah compliant home financing facilities actually work.

This is because a lot of people have been asking me- thus I devote a bit of my time to create this blog post. 🙂

…………………………………..

………………..

………….

In this world, there are 3 types of shariah compliant home financing facilities.

Murabaha

Ijarah Wa Iqtina

Diminishing Musharakah

I will explain from an Islamic Finance practitioner point of view in Singapore, and in layman terms.

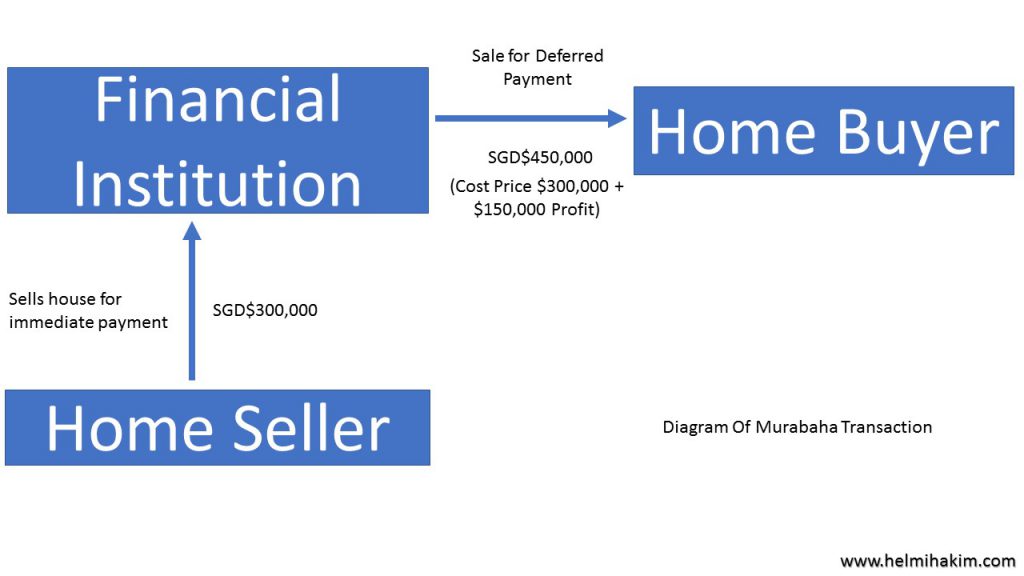

1) Murabaha

In a Murabaha or cost plus financing, you select a property and the financial institution acquires it.

The financial institution adds its profit and sells the asset to you at an agreed upon price on a deferred, usually installment basis.

Its like a shopkeeper who sells you goods on credit.

(Cost Price + Profit), you pay back to the shopkeeper on a deferred, usually installment basis.

This is real trade, in accordance with the Quranic injunction:

‘Allah has permitted trading and forbidden interest’.

This transaction is permissible in Islam.

…..

.

It is important to note that there MUST be a transfer of ownership from the home seller to the financial institution.

Financial Institution must owned the property first,

thenonly it can sell it to you, the home buyer.

This is in conjunction with the hadith of Hakeem ibn Hizaam and ‘Abdullah ibn ‘Amr (may Allah be pleased with them both),

Prophet Muhammad (Peace Be Upon Him) mentioned “Do not sell, what you do not own.”

In Islamic Finance perspective, if the Financial Institution does not own the property, it cannot sell it to you, the home buyer.

………………………………….

………………….

……….

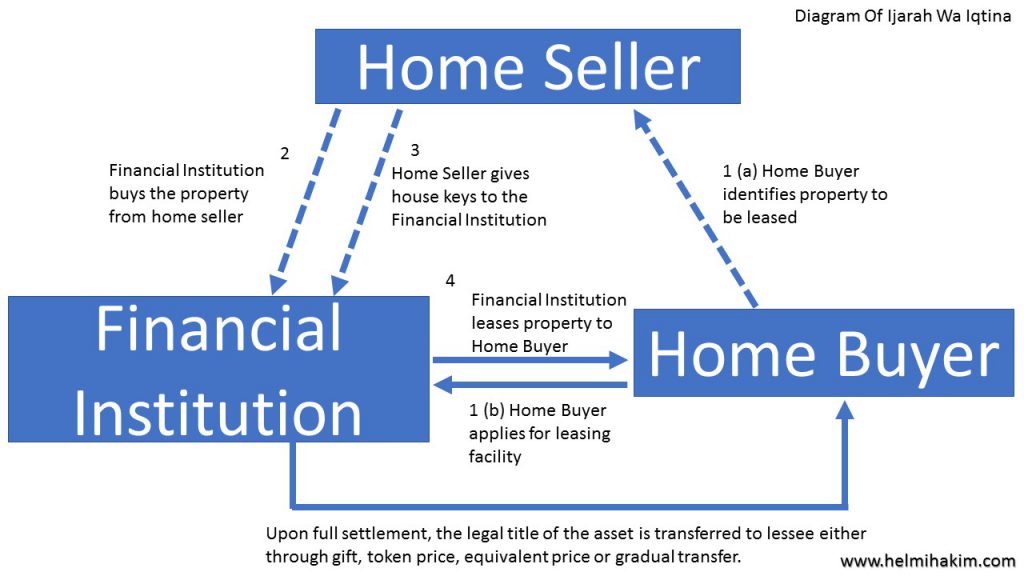

2) Ijarah Wa Iqtina or Ijarah Muntahia Bi’l Tamblik

In an Ijarah or Islamic lease, the financial institution acting as a lessor, buys a property and rents it out to you, the lessee client.

Much later, as part of a seperate agreement, the financial institution offers to sell the property to you. Transfer the ownership to you through gift.

OR ask you to pay the remaining Ijarah instalments before end of lease term

and after that transfer the ownership of property to you through transfer of legal title.

This is permissible in Islam.

………………………………….

………………….

3) Diminishing Musharakah (Musharakah Mutanaqisah)

In a Diminishing Musharakah, the financial institution and you as the home buyer become partners.

Andpurchase the property jointly.

You, as the home buyer move into the property.

Perhaps the property is worth SGD200,000. You pay 10% of the price (SGD20,000) as downpayment.

The Financial Institution takes care of the other 90% of the price (SGD180,000).

This agreement results in 10% home ownership belonging to you, the home buyer.

And the remaining 90% to the Financial Institution.

You then gradually acquire the financial institution’s equity shares in the property.

Until all shares are completely transferred to you.

At the same time, you pay rent in proportion to the financial institution’s remaining equity shares,

with each successive rental payment “diminishing” to the extend of the financial institution’s reduction in its share of the property.

The END result, you will own the property 100% completely, thus no longer needs to pay rental.

At no time, you as the homebuyer pay any interest (riba).

You only pay 2 things.Firstly, the house, in small payments, bit by bit. Secondly, the rent, for the portion of the house which you have not owned yet.

This is permissible in Islam.

(Explanation adapted from Understanding Shari’ah and its application in Islamic Finance (IBIFM) & Ethica Certified Islamic Finance Handbook)

…………………………….

………………….

……………….

As you can see above, the key differencebetween conventional mortgage and a shariah compliant home financing is that conventional mortgage involves loan of cash on interest, whereas a shariah compliant home financingis strictly the exchange of assets.

Each of the above transactions involves an asset and actual ownership by the financial institution. Ultimately, the financial institution must own some (Diminishing Musharakah) or all (Ijarah Wa Iqtina and Murabaha) of the asset for it to be Islamically acceptable.

Insya’Allah, when shariah compliant home financing facility is introduced in Singapore in the near future, I will be exploring strategies on property investment too.

As of now, if you are looking on the practical aspects on how you can save, accumulate and grow your money the shariah compliant way in Singapore, you can always whatsapp/sms me at 96520134 to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

You will want to schedule it asap because I can only accomodate 5 slots per week.

Myth #1: It is EXPENSIVE. It is only reserved for the rich Arabs.

(Arabic Businessmen enjoying a cup of tea)

.

.

Helmi Hakim’s answer: Not true. You can start investing in shariah compliant funds with as little as $5/day or $150/mth.

Gone are the days where shariah compliant instruments are reserved only for the rich and institutional investors with minimal investment amount of $200,000.

Today, common man on the streets in Singapore can also be a shariah compliant investor, with only SGD$150/mth.

………………………………………………

…………………………………..

Myth #2: It is obsolete. It is backward. Some lament that Islamic Finance use ancient strategies. More than 1400 years ago.

Might no longer be applicable today.

Today is modern times. Modern times must use modern investment strategies.

.

.

.

Helmi Hakim’s answer: Not true.

In reality, Islamic Finance have timeless principles as stipulated in the holy Quran and Sunnah of our beloved Prophet Muhammad (Peace and Blessings Be Upon Him) which are relevant and applicable till the day of judgement.

The pertinent principles (no riba, no maysir, no gharar) haven’t change. The application perhaps have changed.

How we apply the pertinent principles essentially does change over time because the modern financial world and business as we know it today is very different to what happened 1400 years ago.

So essentially the modern financial Islamic Finance industry is about taking those crucial, pertinent principles.

And apply them in the modern context.

No riba. No Maysir. No Gharar. In the context of the 21st Century.

In fact, I can argue that most global financial problems in the world today happens because of Riba (Interest), Maysir (Speculation) and Gharar (Uncertainty).

Be it the subprime mortgage crisis in year 2008, the Asian financial crisis in year 1997, Euro Debt Crisis, 1MDB saga, anything you can think of.

Allah S.W.T. has given us the prescriptions to the global economic ailments in the holy Quran and sunnah of our beloved Prophet Muhammad (Peace and Blessings Be Upon Him). Why don’t we just follow them?

Of course, if I were to lay down everything here, my post will never end.

You can schedule a free consultation session with me to discuss more. Insya’Allah. 🙂

……………………………………………

…………………………..

Myth #3: It is FAKE.

Yek Eleh… They just replace the word “interest” with the word “profits”.

It is still conventional. But just dressed up as Halal.

.

.

.

Helmi Hakim’s answer: Not true.

Name me any Islamic financial contracts. In essence, all of them are free from riba (interest), maysir and gharar.

Let me explain with a simple example.

Example, I set up a chicken rice stall.

Alhamdulillah.

My chicken rice is delicious.

A lot of customers queue to buy my chicken rice every day.

As a businessman, because I have one chicken rice stall that is so profitable, I want to expand my business.

I want to open up more stalls selling my delicious chicken rice.

Perhaps now my stall is in Tampines.

(Copyright belongs to Google Map)

I want to open one in Punggol, one in Pasir Ris, one in Woodlands, one in Jurong West and one in Somerset.

But, I dont have much money.

So what I do, I become a bond issuer. I approach people like yourself.

You give me $100,000.

I promise you that every quarter, or every half year or perhaps every year, I will give you money.

Regardless, my new chicken rice stall makes money OR lose money, I will still give you money.

The money that I give you is called coupons.

From shariah compliant perspective, the coupons is not permissible because it is still known as interest and essentially riba.

……………………………………………..

………………………

…………….

So how do we do it the shariah compliant way?

Again, I approach you.

This time round, I invite you to be my business partner in this new stall.

You run the stall for me.

I share with you my secret delicious chicken rice recipe.

At the end of the day, we share our profit and loss.

You take 70%, I take 30%. This is allowed from shariah perspectives. In Islamic Finance, it is known as Musharakah.

………………………

………………

….

For another stall, I approach my friend.

This time round, my friend told me that he doesn’t want to run the stall.

But he wants to be an INVESTOR.

Okay. He contributes $50,000 to my new stall.

This time round, we have an agreeable profit sharing ratio.

Perhaps, I take 70% and he takes 30%.

However, if our business loses money, my friend’s loss will be limited to the $50,000 capital that he contributed.

This is allowed from shariah perspectives. In Islamic Finance, it is known as Mudarabah.

Based on the above example,

I just like to illustrate that the application of Islamic Finance in our daily lives is REAL.

It is not just simply dressing up something that is haram to something that is Halal.

……………………………………………………….

………………………………………

Myth #4: It is DIFFICULT to understand.

It is too exotic. Too mysterious. Too unknown.

Mudarabah? Murabaha? Musharakah? Ijarah Muntahia Bithambleek?

Very confusing…

.

.

.

Helmi Hakim’s answer:

Well. The Malay proverb says, “Alah bisa, tegal biasa”.

Anything we do for the first time might feel difficult.But if we do it a lot of times, it becomes easier.

Because it becomes familiar and second nature to us.

In fact, when I first started my journey as a financial consultant in year 2007, I have ZERO educational background in Islamic Finance.

I had Diploma in Accountancy from Ngee Ann Polytechnic.

Sure! You asked me on how to interpret financial statements back then, Insya’Allah, I would be able to assist you.

But you asked me about Islamic Finance, I will stare at you with a blank face.

At that point, I just relied on the Fatwas by MUIS, our religious authority in Singapore. Nothing more than that.

Gradually, I upgrade myself.

I took my degree, Bachelor Of Science (Hons) Banking and Wealth Management with University of Wales (UK).

They have a module on Islamic Finance.

Then, I took an Islamic Finance Certification with Australia Islamic Finance Centre (AUCIF).

Currently, I am studying for my exams, Certified Islamic Finance Executive by Ethica Institute which is based in Dubai.

The point, I am trying to bring across is that we have to start somewhere. A journey of a thousand miles began with the first step. The first step towards the right direction.

Insya’Allah, if we have set our niat right, Allah S.W.T. will guide us, show us the path and make it easier for us.

So, get started! 🙂

.

.

.

Myth #5: It is troublesome/leceh/mafan.

Make money, make money only lah. Religion should be set aside.

No need to distinguish whether it is Halal or Haram.

As long we can make money, it is for the greater good right? Why need to think too hard?

.

.

Helmi Hakim’s answer:

There are 2 ways of making money.

The shariah compliant (halal) way. And the non shariah compliant way. If you can make money the shariah compliant way, why do it the non-shariah compliant way?

At the end of the day, you still make moneyright? 🙂

…………………

….

To say that making money the shariah compliant way in Singapore is troublesome is not true at all.

In fact, the basic fundamentals of how shariah compliant fund makes money and non-shariah compliant funds make money is the about the SAME.

The only difference is the underlying assets.

To do it the shariah compliant way, the underlying asset has to be shariah compliant.

No pork. No alcohol. No casinos.

And other pertinent requirements (absence of riba, maysir and gharar) to ensure that the financial transaction and the underlying assets are permissible in Islam. Shariah compliant. Halal wa Thoyibban.

As Muslims, the practise of our beloved religion, Islam covers all aspects of our life.

Family. Community. Business.

To Ibadah. Morals and even areas such as our personal hygiene.

Islam does not adopt a secular model whereby religion plays little or no role in public affairs.

There is no segregation of ‘church’ and ‘state’ as such. Religion and our daily lives goes hand in hand! 🙂

Above are just some myths that I came across when meeting hundreds of Singaporean Muslims out there, to share on how they can plan their finance, the shariah compliant way in Singapore.

If you are looking on the practical aspects on how you can save, accumulate and grow your money the shariah compliant way in Singapore, you can always whatsapp/sms me at 96520134 to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

You will want to schedule it asap because I can only accomodate 5 slots per week.

Time flies.

Today is already the last few days we Muslims celebrate Hari Raya Puasa. 🙂

Every Hari Raya Puasa is special to me.

Nevertheless, this year Hari Raya Puasa is EXTRAspecial to me.

This is because Alhamdulillah….

It is the first Hari Raya my wife and I celebrate with our 3 months old baby, Yaslyn Inara. 🙂

(Myself, my wife and my baby)

Her laughter. Her cries. Her comel (super cute) cutie pie face melts my heart.

And it is such a joy looking at her cheeky and innocent smile (especially when she feels good after we clean and change her diapers).

………………………………..

……………………..

……………

Hari Raya Puasa brings a lot of memories to me.

And below are 3 things I like about Hari Raya Puasa most and how it relates to Islamic Financial Planning in Singapore. 🙂

…………………………………………………

…………………………….

………………..

1) Takbir Raya

I always look forward to the melodic tune of takbir raya, as I am deeply moved by the meaning of it. Takbir raya never fails to touch my heart.

……………………….

…………….

Allahu Akbar. Allahu Akbar. Allahu Akbar.

Allah is great. Allah is great. Allah is great.

La ilaha illallah Allahu Akbar, Allahu Akbar walilahi ilhamd

There is no God, but Allah Allah is Great, Allah is Great; to Him belongs all Praise

It reminds me that no matter how great or how grand we plan our finances or our business,

Allah S.W.T. is the master, the best of all planners.

Allah S.W.T. is the greatest.

We can put in 99% of our effort to plan and work wholeheartedly to achieve our goals.

But if Allah S.W.T does not grant us that 1%, we will never achieve the goals that we plan and work for.

We can work 13-14 hours a day to achieve our financial/business goals.

But without Allah’s blessing, our financial/business goals will remain a distant dream.

.

So remember, in everything we plan for.

Be it our financial goals.

Our business goals.

Our relationship goals.

Make doa to Allah S.W.T. that Allah S.W.T. helps us to achieve them.

After that, put in MASSIVE effort and tawakkal.

……………………………………………………………………..

……………………………………………….

…………………………

2) Hari Raya Visiting

Hari Raya is also that time of the year where you get to visit your family members.

Visiting relatives is a great practice to strengthen the ukhwah or bond between families.

After all, families are the founding blocks of any society.

If we’re not peaceful or loving at this level, how do expect the ummah to be peaceful and loving also? 🙂

……………………………………..

………………………

It’s also a great time to catch up on everyone’s lives and at the same time, seek forgiveness for any transgressions that had happened over the year.

Sometimes we may think we have no problem with our aunts or cousins etc, but perhaps there may have been a time where your words had unknowingly hurt them.

In the Quran, Allah encourages us to forgive one another if we expect His forgiveness.

So what better way to start than seeking forgiveness from your own family members?

This practice helps gel the relationship between family members.

(My relatives who are amongst the first few visitors to my house)

………………………………………………….

……………………………………

…………………….

In fact, many times during my Islamic Financial Planning, I emphasize the importance of silaturahmi.

Anas ibn Malik reported: The Messenger of Allah, peace and blessings be upon him, said, “Whoever is pleased to have his provision expanded and his life span extended, then he should keep good relations with his family.”

Source: Sahih al-Bukhari 1961, Sahih Muslim 2557

.

.

Prophet Muhammad (Peace Be Upon Him) said: “No person severs ties of kinship would enter Paradise.”

[Reported by Muslim 2556]

.

.

“Learn enough about your lineage to facilitate keeping your ties of kinship. For indeed keeping the ties of kinship encourages affection among the relatives, increases the wealth, and increases the lifespan.”

(HR Imam Tirmidzi)

……………………………………………….

………………………………….

………………………

…………

……

3) The Joy Of Giving Duit Raya

Yes. As a kid, I love to go Hari Raya because I get Duit Raya.

We jokingly refer that as “Duit Raya Collection”. 🙂

(My daughter’s duit raya for this Shawal)

……..

.

When we are adults now, we’re no longer collecting but giving.

There’s joy in giving out duit raya.

It’s such a pleasure to see the bright smiles of kids with their laughters. 🙂

But you don’t only give the kids.

If you’re able to afford it, don’t forget to gift your elders with duit raya too.

The appreciative looks of our elders will warm the heart; you’re not only making them happy but you’re also racking up points on your good deeds scale, Insya’Allah.

…………………………………………………………………………..

……………………………………………………..

………………………………….

In Islamic Financial Planning, I advocate not only paying our obligatory zakat, but also making more donations.

During Ramadan, we’re always making conscious effort to donate, because we know the blessed month carries hefty rewards.

During Hari Raya, the practice of duit raya is also a form of donation.

But outside these months, at times, some of us tend to lax a bit on donations.

So a good practice in Islamic Financial Planning is to make conscious donations.

Perhaps you may want to consider setting up auto GIRO deduction for one or a few charitable organizations. This will be part of your monthly budget, which your financial planner can help draw up.

For all my clients, you know that you have an option to donate a specific percentage of your monthly premium contribution to charity.

(My clients have an option to donate part of their monthly premiums to charity)

………………………………………………………

………………………………

In my Islamic Financial Planning, I share the importance and benefits of donating your money.

Abdullah ibn Umar reported: Prophet Muhammad (Peace And Blessings Be Upon Him) was upon the pulpit mentioning charity and abstaining from begging and he said, “The upper hand is better than the lower hand, the upper hand being the one that gives and the lower hand being the one that receives.”

Source: Sahih Muslim 1033

.

.

Prophet Muhammad (Peace and Blessings Be Upon Him) said: “Allah loves the God-fearing rich man [who gives much in charity but still] remains obscure and uncelebrated.” (Muslim)

.

.

At the end of the day, we not only want to accumulate our wealth. We seek baraqah in it.

We pray that we get blessings from Allah S.W.T. in whatever we do,

especially when its comes to work for our rezeki on this earth.

……………………………………………….

…………………..

………..

That sums up the 3 things I like about Hari Raya Puasa and how it relates to Islamic Financial Planning in Singapore.

If you are looking on the practical aspects on how you can save, accumulate and grow your money the shariah compliant way in Singapore,

you can always whatsapp/sms me at 96520134 to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

You will want to schedule it asap because I can only accomodate 5 slots per week.

And next week, I will be heading for my long holiday to Oman and Dubai. Insya’Allah.

One of my personal goals for year 2017 is to hit my first MDRT (Million Dollar Round Table), the shariah compliant way.

By reaching out to Muslim families in Singapore who like to plan their finance, the halal way. The shariah compliant way.

That is my personal goal. To achieve your own personal goals, you need strategies.

Here are 3 important questions you have to ask yourself first to uncover proven, confirm to work strategies that can help you achieve your goals.

1) What new knowledge/skills do you need?

2) Who can help you achieve your goals?

3) How do you achieve your goals faster?

……………………………………………………………………

……………………………………………….

……………………..

1. WHAT new knowledge/skills do you need?

There is a saying, “INSANITY is doing the same thing over and over again and expecting different results.”

Which means you cannot just rely on whatever knowledge and skills you have now.

Life is a constant learning journey: the arrogant is he who thinks he knows or has everything he needs to succeed.

Once you start to seriously move towards your goals, you’ll realize you’ll need new knowledge or skill.

Sit down for a moment and really think through this question.

What new knowledge/skills do you need? 🙂

Personally for me to achieve my MDRT, these are the new knowledge and skills that I need.

I need to acquire knowledge on how to attract qualified leads. It can be online or offline strategies.

I need to upgrade my knowledge on Islamic Finance. Sure, I took an Islamic Finance module during my degree

.

.

..

And Islamic Finance Certification with Australia Centre For Islamic Finance few years back.

.

. . It is time to refresh and upgrade myself with a new Islamic Finance certification for year 2017! The industry is changing rapidly, and getting an additional certification will bolster my knowledge and effort to advice my clients better.

2. WHO can help you achieve your goals?

There’s a famous saying: No man is an island.

We cannot possibly do things on our own.

Our knowledge, skill and understanding of the world is limited. We will need help. With the example of saving up, who do you think can best help you achieve your goals?

Maybe you can approach a financial planner (or me! hehehe).

And together we work out the best plan to to achieve your goal. 🙂

Or perhaps your spouse can help keep you accountable. If you know you can’t be disciplined to save, then she can be the ‘unofficial’ banker.

This might mean going to her every month and asking her to help hold on to the money you plan to save.

………………………………….

…………………..

…….

For me personally, to achieve my MDRT, I look for qualified people that can help me achieve my goals too. I surround myself with these people.

– This year itself, I have signed up for Ethica’s Certified Islamic Finance Executive™ (CIFE™) course.

Ethica’s Certified Islamic Finance Executive™ (CIFE™) is a globally recognized certificate accredited by scholars to fully comply with AAOIFI, the world’s leading Islamic finance standard.

Till date, I do not know of any practicing financial planner in Singapore who are trained AAOIFI compliant certifications. AAOIFI compliant is the de facto standard in over 90% of the world’s jurisdictions. Let me be the FIRST amongst the 20,000 financial planners in Singapore! Insya’Allah… 🙂

…………………

……………………..

..

– I have also signed up, for an online marketing 2 days practical workshop, where I will learn more on facebook marketing. Many of you today, my blog readers are already my clients.

You get to know me over the internet after reading my blog posts or viewing my youtube videos.

Insya’Allah, I will find qualified people to help me, in my mission to spread the goodness of Islamic Finance to our fellow Singaporeans.

Let us make every single step to find rezeki in the world, an ibadah. May our efforts benefit us in this world, and hereafter. Insya’Allah…

……………..

……..

….

– Next week, I am meeting my lawyers to discuss further on trademarks, that I will register for my signature programs, “Unlock Your Money” session and “Your Financial M.A.P.” session.

I first learnt about trademarks and copyrights, when I was a full time student in Ngee Ann Polytechnic many years back.

I took Business Law as one of the modules, while undertaking Diploma In Accountancy.

Little did I know, many years later, I would be liaising with lawyers to register my own personal trademarks. Exciting!!! 🙂

…………………………………

……………………….

…………….

– I have also reached out to my Arab teacher in Egypt, where I will continue back learning Arabic Language via Skype with him every Monday, after Subuh prayers.

In my opinion, the best time time to learn or memorise something, is before you sleep, and after you wake up.

Learning Arabic Language has been very tough for me.

It is no easy feat. :/

Pray for me that I will istiqamah in my journey to learn how to read, understand and speak Arabic Language with confidence. Insya’Allah! 🙂

3. HOW do you achieve your goals faster?

Alright, you’re almost ready to make your goals come true.

So the 3rd question you should ask yourself is how do you achieve your goals faster?

I like to add some buffer, whenever I set my goals.

So even though, I target to achieve MDRT for year 2017….. I shall target to achieve my MDRT by 31st October 2017, which happens to be my birthday! 🙂

But how? Easier said than done! 🙂

…………………………………………………………

…………………………………………..

……………………………………..

I remembered, one of the quotes of wisdom, by a Singaporean entrepreneur, Sant Qiu, “Whatever you can do, you can do it bigger, better, faster…… with the right team. So assemble the right team as early as you can and achieve bigger, better results faster.”

………………………………………………………………..

………………………………………..

………………………..

You might have heard about Robo Advisor.

I am in the process of creating my own personal shariah compliant Robo Advisor.

I will also be engaging para planners.

They will work hand in hand with me to assist me in developing comprehensive, powerful shariah compliant financial planning strategies for my clients in Singapore.

My team will comprise of robots and humans.

We will alter the history of the financial planning industry in Singapore, the way financial planners run our financial practice in Singapore.

By introducing my personal, revolutionary financial planning practice hybrid model- that combines the best of high-tech and high-touch.

It never happen before, and change is inevitable.

In fact, the process has already begun. You might have heard about Takaful.sg

That is one of my fintech intiatives, which is already “live” in Singapore.

Many, many, more exciting things to come! 🙂

So, there I cover 3 important questions you have to ask yourself first to uncover proven, confirm to work strategies that can help you achieve your goals.

1) What new knowledge/skills do you need?

2) Who can help you achieve your goals?

3) How do you achieve your goals faster?

……………………………………………………………………

………………………………………………

………………….

If you like to receive undivided attention from me as a financial planner, to help you plan your finance the shariah compliant way in Singapore, you can schedule an appointment with me here. Or just whatsapp/SMS me direct at 96520134.

Because of my busy schedule, I can only accommodate additional 5 slots every week, so do click the link, and schedule an appointment with me now.

A certified financial consultant, Helmi Hakim has won praise for his patience, perseverance and practicality when solving his clients’ financial concerns. For more information on how you can manage your finances better, contact Helmi Hakim at 96520134.