“Helmi Hakim. I want to buy a house in Singapore. I dont have money to pay full in cash thus I have to take a loan.

Is there shariah compliant home financing facility in Singapore?”

………………………………..

………………

……….

I have made it clear that there is NO shariah compliant home financing facility in Singapore at this point of time.

That’s why I created Takaful.sg with my unique Your Financial M.A.P. Model™ to share simple yet powerful strategies on how you can clear your Riba Based loans in Singapore.

In this blog post, I am going to share with you how shariah compliant home financing facilities actually work.

This is because a lot of people have been asking me- thus I devote a bit of my time to create this blog post. 🙂

…………………………………..

………………..

………….

In this world, there are 3 types of shariah compliant home financing facilities.

Murabaha

Ijarah Wa Iqtina

Diminishing Musharakah

I will explain from an Islamic Finance practitioner point of view in Singapore, and in layman terms.

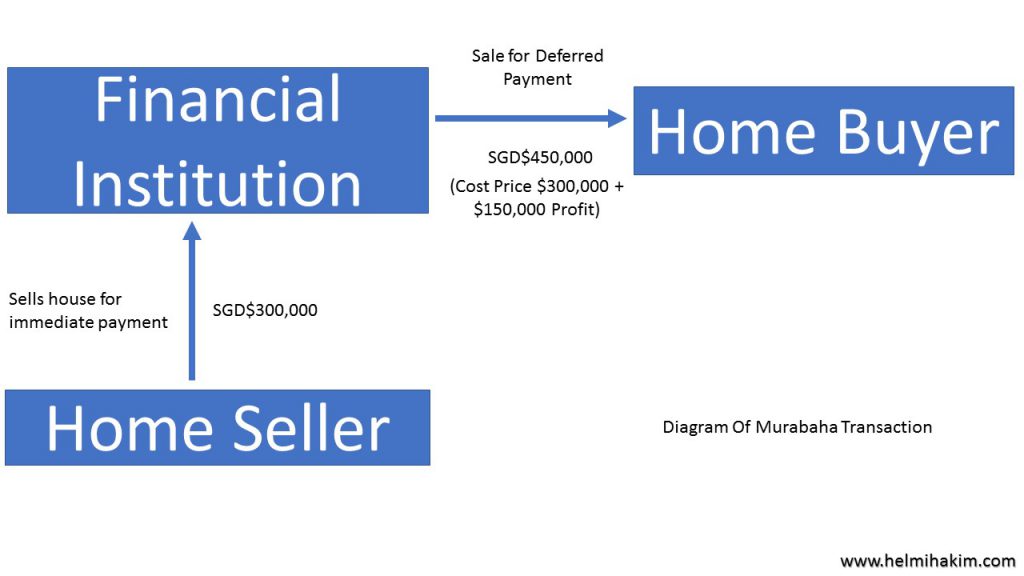

1) Murabaha

In a Murabaha or cost plus financing, you select a property and the financial institution acquires it.

The financial institution adds its profit and sells the asset to you at an agreed upon price on a deferred, usually installment basis.

Its like a shopkeeper who sells you goods on credit.

(Cost Price + Profit), you pay back to the shopkeeper on a deferred, usually installment basis.

This is real trade, in accordance with the Quranic injunction:

‘Allah has permitted trading and forbidden interest’.

This transaction is permissible in Islam.

…..

.

It is important to note that there MUST be a transfer of ownership from the home seller to the financial institution.

Financial Institution must owned the property first,

thenonly it can sell it to you, the home buyer.

This is in conjunction with the hadith of Hakeem ibn Hizaam and ‘Abdullah ibn ‘Amr (may Allah be pleased with them both),

Prophet Muhammad (Peace Be Upon Him) mentioned “Do not sell, what you do not own.”

In Islamic Finance perspective, if the Financial Institution does not own the property, it cannot sell it to you, the home buyer.

………………………………….

………………….

……….

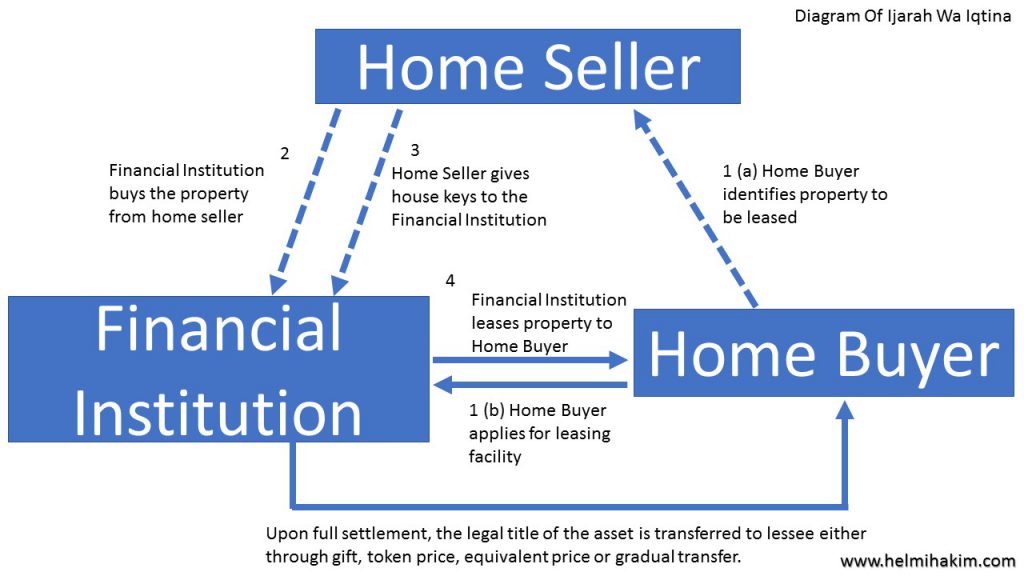

2) Ijarah Wa Iqtina or Ijarah Muntahia Bi’l Tamblik

In an Ijarah or Islamic lease, the financial institution acting as a lessor, buys a property and rents it out to you, the lessee client.

Much later, as part of a seperate agreement, the financial institution offers to sell the property to you. Transfer the ownership to you through gift.

OR ask you to pay the remaining Ijarah instalments before end of lease term

and after that transfer the ownership of property to you through transfer of legal title.

This is permissible in Islam.

………………………………….

………………….

3) Diminishing Musharakah (Musharakah Mutanaqisah)

In a Diminishing Musharakah, the financial institution and you as the home buyer become partners.

Andpurchase the property jointly.

You, as the home buyer move into the property.

Perhaps the property is worth SGD200,000. You pay 10% of the price (SGD20,000) as downpayment.

The Financial Institution takes care of the other 90% of the price (SGD180,000).

This agreement results in 10% home ownership belonging to you, the home buyer.

And the remaining 90% to the Financial Institution.

You then gradually acquire the financial institution’s equity shares in the property.

Until all shares are completely transferred to you.

At the same time, you pay rent in proportion to the financial institution’s remaining equity shares,

with each successive rental payment “diminishing” to the extend of the financial institution’s reduction in its share of the property.

The END result, you will own the property 100% completely, thus no longer needs to pay rental.

At no time, you as the homebuyer pay any interest (riba).

You only pay 2 things.Firstly, the house, in small payments, bit by bit. Secondly, the rent, for the portion of the house which you have not owned yet.

This is permissible in Islam.

(Explanation adapted from Understanding Shari’ah and its application in Islamic Finance (IBIFM) & Ethica Certified Islamic Finance Handbook)

…………………………….

………………….

……………….

As you can see above, the key differencebetween conventional mortgage and a shariah compliant home financing is that conventional mortgage involves loan of cash on interest, whereas a shariah compliant home financingis strictly the exchange of assets.

Each of the above transactions involves an asset and actual ownership by the financial institution. Ultimately, the financial institution must own some (Diminishing Musharakah) or all (Ijarah Wa Iqtina and Murabaha) of the asset for it to be Islamically acceptable.

Insya’Allah, when shariah compliant home financing facility is introduced in Singapore in the near future, I will be exploring strategies on property investment too.

As of now, if you are looking on the practical aspects on how you can save, accumulate and grow your money the shariah compliant way in Singapore, you can always whatsapp/sms me at 96520134 to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

You will want to schedule it asap because I can only accomodate 5 slots per week.

Alhamdulillah. I just finished my 2-week army reservist. 🙂

Being in vegetation for a while with combat rations as my food supply, I was deprived of good food.

Many types of food ran into my mind.

Nasi Campur Sinar Cahaya at Pasar Geylang Serai

Roti John Steak Mama Power @ Old Woodlands

Epok Epok Ganja @ 1 Bedok Road

Everything seems so delicious at that point of time! … and then comes, this Nasi Lemak Burger by Macdonalds… 🙂

Okay lah. This is something unique.

Malay food combined with Western Food.

Nasi Lemak combined with burger.

…………………………….

…………….

Never tried before.

So the first thing I did after I outpro and relaxed at home, was to chill at Macdonalds with my wife, sharing a Nasi Lemak Burger.

As I unwrapped my burger… a nice hint of the smell of santan greeted me….

and then out came the coconut flavoured chicken thigh patty, fried egg, caramelised onions, two slices of cucumber and a smear of sambal.

Those who have tried this burger definitely would agree with me, what makes this burger special is the sambal.

The sambal is amazing!

The sweet, spicy cameralised onion sambal is so refreshing, tantalised my tastebuds, and reminded me of the RM1.50 roadside Makcik Nasi Lemak at Johor Bahru.

Sweet, yummy sambal wrapped together with Nasi Lemak in banana leaves and Utusan Malaysia newspaper.

Difficult to find in Singapore, this kind of Nasi Lemak.

Overall, I will give Macdonald Nasi Lemak burger 5/5.

……………………………………….

………………

……….

This Nasi Lemak Burger also serves as a learning lesson for Islamic Finance Practitioners in Singapore.

Nasi Lemak Burger combines the BEST of Malay food – Nasi Lemak – and the BEST of Western food – burgers.

Islamic Finance Practioners can combine the BEST practices in Islamic Financial Planning and Conventional Financial Planning.

Let me explain and give practical examples.

………………………………………………………………………………

…………………………………

For Islamic Financial Planning, we save our contingency/emergency funds in Al Wadiah Savings Account.

Alhamdulillah, we know it is shariah compliant because it gives Hibah instead of Interest.

How much to save as contingency funds?

Best practices in conventional finance is to adopt a basic liquidity ratio of 3-6 months.

It means you can have 3-6 months of your monthly expenses in your Al Wadiah Savings account.

……………………………………

…………………….

…………

In Islamic Financial Planning, we know in order to buy a house, the shariah compliant way is to use Murabahah, Diminishing Musharakah or Ijarah Wa Iqtina financing facilities.

In the future, once shariah compliant home financing is available in Singapore, we don’t overleverage and immediately

buy properties worth millions of dollars.

Take millions of dollars of shariah compliant financing because it is shariah compliant.

No. We dont do that.

We follow the best practices in conventional finance which is to follow closely this ratio known as, Total Debt Service Ratio (TDSR).

TDSR= Total Debt Yearly Repayment/Annualised Take Home Pay

This ratio measures the proportion of take home income, used to make regular payment of debts.

If it is lower than 35%, means HEALTHY.

It means that there is sufficient take home pay available to service debt repayments.

A ratio of 45% or above for this ratio is generally considered unhealthy and may risk of not being able to service these regular debt repayments.

Follow the recommended TDSR guidelines, even though if the financing facilities are shariah compliant.

Dont overleverage.

…………………………………………………

…………………………….

…………………..

When you invest your money the shariah compliant way for your retirement, you can follow certain personal financial ratio guidelines.

…………………..

.

Savings Ratio = Savings/Gross Income

This ratio calculate the proportion of your income, you set up for savings. You need to save at least minimum 10% of your gross income.

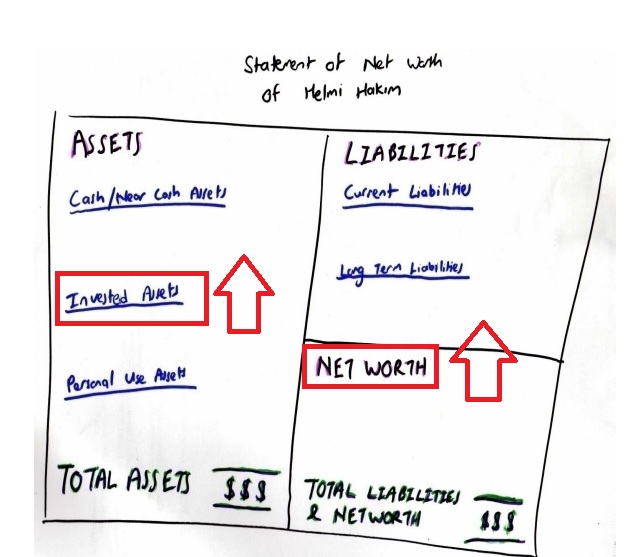

Investment Assets To Net Worth Ratio = Invested Assets/Networth

This ratio compares the value of invested assets with networth.

An individual should have clear targets on accumulating capital for the longer term, excluding investment in the house that you are staying in.

The target is to have sufficient assets accumulated for retirement and other financial purposes.

If it is more than 50%, means HEALTHY.

……………………………………………….

………………………..

……..

Above are just some best practices in conventional finance that I personally adopt to my Islamic Financial Planning services.

If you are looking on the practical aspects on how you can save, accumulate and grow your money the shariah compliant way in Singapore,

you can always whatsapp/sms me at 96520134 to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

You will want to schedule it asap because I can only accomodate 5 slots per week.

And next week, I will be heading for my long holiday to Oman and Dubai. Insya’Allah.

Time flies.

Today is already the last few days we Muslims celebrate Hari Raya Puasa. 🙂

Every Hari Raya Puasa is special to me.

Nevertheless, this year Hari Raya Puasa is EXTRAspecial to me.

This is because Alhamdulillah….

It is the first Hari Raya my wife and I celebrate with our 3 months old baby, Yaslyn Inara. 🙂

(Myself, my wife and my baby)

Her laughter. Her cries. Her comel (super cute) cutie pie face melts my heart.

And it is such a joy looking at her cheeky and innocent smile (especially when she feels good after we clean and change her diapers).

………………………………..

……………………..

……………

Hari Raya Puasa brings a lot of memories to me.

And below are 3 things I like about Hari Raya Puasa most and how it relates to Islamic Financial Planning in Singapore. 🙂

…………………………………………………

…………………………….

………………..

1) Takbir Raya

I always look forward to the melodic tune of takbir raya, as I am deeply moved by the meaning of it. Takbir raya never fails to touch my heart.

……………………….

…………….

Allahu Akbar. Allahu Akbar. Allahu Akbar.

Allah is great. Allah is great. Allah is great.

La ilaha illallah Allahu Akbar, Allahu Akbar walilahi ilhamd

There is no God, but Allah Allah is Great, Allah is Great; to Him belongs all Praise

It reminds me that no matter how great or how grand we plan our finances or our business,

Allah S.W.T. is the master, the best of all planners.

Allah S.W.T. is the greatest.

We can put in 99% of our effort to plan and work wholeheartedly to achieve our goals.

But if Allah S.W.T does not grant us that 1%, we will never achieve the goals that we plan and work for.

We can work 13-14 hours a day to achieve our financial/business goals.

But without Allah’s blessing, our financial/business goals will remain a distant dream.

.

So remember, in everything we plan for.

Be it our financial goals.

Our business goals.

Our relationship goals.

Make doa to Allah S.W.T. that Allah S.W.T. helps us to achieve them.

After that, put in MASSIVE effort and tawakkal.

……………………………………………………………………..

……………………………………………….

…………………………

2) Hari Raya Visiting

Hari Raya is also that time of the year where you get to visit your family members.

Visiting relatives is a great practice to strengthen the ukhwah or bond between families.

After all, families are the founding blocks of any society.

If we’re not peaceful or loving at this level, how do expect the ummah to be peaceful and loving also? 🙂

……………………………………..

………………………

It’s also a great time to catch up on everyone’s lives and at the same time, seek forgiveness for any transgressions that had happened over the year.

Sometimes we may think we have no problem with our aunts or cousins etc, but perhaps there may have been a time where your words had unknowingly hurt them.

In the Quran, Allah encourages us to forgive one another if we expect His forgiveness.

So what better way to start than seeking forgiveness from your own family members?

This practice helps gel the relationship between family members.

(My relatives who are amongst the first few visitors to my house)

………………………………………………….

……………………………………

…………………….

In fact, many times during my Islamic Financial Planning, I emphasize the importance of silaturahmi.

Anas ibn Malik reported: The Messenger of Allah, peace and blessings be upon him, said, “Whoever is pleased to have his provision expanded and his life span extended, then he should keep good relations with his family.”

Source: Sahih al-Bukhari 1961, Sahih Muslim 2557

.

.

Prophet Muhammad (Peace Be Upon Him) said: “No person severs ties of kinship would enter Paradise.”

[Reported by Muslim 2556]

.

.

“Learn enough about your lineage to facilitate keeping your ties of kinship. For indeed keeping the ties of kinship encourages affection among the relatives, increases the wealth, and increases the lifespan.”

(HR Imam Tirmidzi)

……………………………………………….

………………………………….

………………………

…………

……

3) The Joy Of Giving Duit Raya

Yes. As a kid, I love to go Hari Raya because I get Duit Raya.

We jokingly refer that as “Duit Raya Collection”. 🙂

(My daughter’s duit raya for this Shawal)

……..

.

When we are adults now, we’re no longer collecting but giving.

There’s joy in giving out duit raya.

It’s such a pleasure to see the bright smiles of kids with their laughters. 🙂

But you don’t only give the kids.

If you’re able to afford it, don’t forget to gift your elders with duit raya too.

The appreciative looks of our elders will warm the heart; you’re not only making them happy but you’re also racking up points on your good deeds scale, Insya’Allah.

…………………………………………………………………………..

……………………………………………………..

………………………………….

In Islamic Financial Planning, I advocate not only paying our obligatory zakat, but also making more donations.

During Ramadan, we’re always making conscious effort to donate, because we know the blessed month carries hefty rewards.

During Hari Raya, the practice of duit raya is also a form of donation.

But outside these months, at times, some of us tend to lax a bit on donations.

So a good practice in Islamic Financial Planning is to make conscious donations.

Perhaps you may want to consider setting up auto GIRO deduction for one or a few charitable organizations. This will be part of your monthly budget, which your financial planner can help draw up.

For all my clients, you know that you have an option to donate a specific percentage of your monthly premium contribution to charity.

(My clients have an option to donate part of their monthly premiums to charity)

………………………………………………………

………………………………

In my Islamic Financial Planning, I share the importance and benefits of donating your money.

Abdullah ibn Umar reported: Prophet Muhammad (Peace And Blessings Be Upon Him) was upon the pulpit mentioning charity and abstaining from begging and he said, “The upper hand is better than the lower hand, the upper hand being the one that gives and the lower hand being the one that receives.”

Source: Sahih Muslim 1033

.

.

Prophet Muhammad (Peace and Blessings Be Upon Him) said: “Allah loves the God-fearing rich man [who gives much in charity but still] remains obscure and uncelebrated.” (Muslim)

.

.

At the end of the day, we not only want to accumulate our wealth. We seek baraqah in it.

We pray that we get blessings from Allah S.W.T. in whatever we do,

especially when its comes to work for our rezeki on this earth.

……………………………………………….

…………………..

………..

That sums up the 3 things I like about Hari Raya Puasa and how it relates to Islamic Financial Planning in Singapore.

If you are looking on the practical aspects on how you can save, accumulate and grow your money the shariah compliant way in Singapore,

you can always whatsapp/sms me at 96520134 to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

You will want to schedule it asap because I can only accomodate 5 slots per week.

And next week, I will be heading for my long holiday to Oman and Dubai. Insya’Allah.

Alhamdulillah. Ramadan is a blessed guest that comes once a year.

In this beautiful month, we Muslims are encouraged to increase our worship

and to be more charitable.

It’s a month filled with barakah, where your deeds are multiplied.

And your sins will be forgiven if you are sincere.

When we abstain from food and drink, it’s a reminder to be mindful of those around us who are less fortunate.

We also have to watch our words and temper. Ramadan helps us to develop our better self.

So don’t be surprise some of our best practices in Ramadan are also useful principles in managing your personal finances.

I termed the concept with the acronym R.A.M.A.D.A.N. so that it is easier to remember. 🙂

Reflect

Ramadan is a time of reflection.

It is a time for introspection.

It is a time where we should take stock of ourselves.

And have an honest assessment of our shortcomings.

It is the time of the year in which we recharge our iman.

And prepare for the challenges facing us over the next 334 days.

Challenges that will test us in the next 8016 hours.

Getting ourselves prepared every single moment.Every single 480,960 minutes to come!

This can only be done if we muhasabah…. pause, reflect on our own faults,

introduce feedforward controls

and implement solutions during this important month.

(Beautiful side view of Sultan Mosque)

……………………………………..

…………………………..

…………..

Similar to managing our personal finance, we should reflect and ask ourselves these questions.

Do I have 3-6 months of emergency expenses in my bank account? (Basic Liquidity Ratio)

Have I been saving 20% of my monthly income? (Savings Ratio)

Is my debt service ratio above the recommended rate? Am I highly leverage?

And most importantly, from a perspective of a Muslim, we need to reflect on this.

Have I been paying zakat for my cooperative insurance policies

and shariah compliant investable assets when it hits the nisab value and reach the haul of 1 year?

……………………………………………………

…………………………………

…………………………..

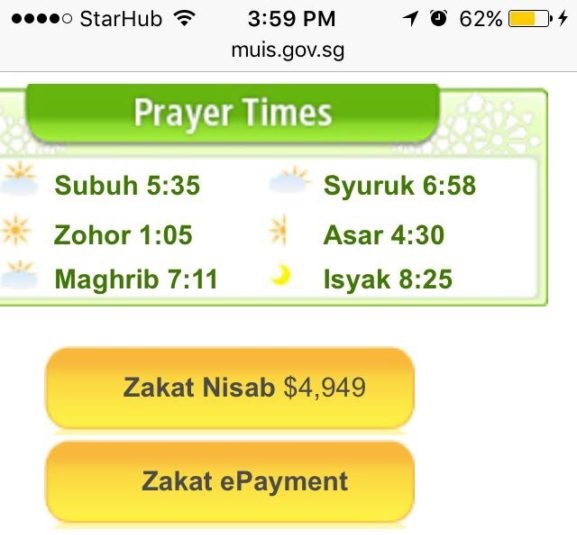

(The kadar nisab as of today, 11th June 2017)

……………………………………………..

……………………………

……………….

These are important questions that you have to ask yourself.

.

The reason why I am bringing this up is because I just received a call from one of my blog readers.

She told me, she paid for zakat fitrah all along. BUT she has OVERLOOKED paying her zakat harta for her cooperative insurance policies and shariah compliant investable assets for the past 20 years!

Paying zakat is one of the pillars of Islam.

She is clueless and seeked my advice on what she could do.

Of course, now is the best time for us to reflect on ourselves too! 🙂

…………………………………………….

………………………….

…………………

Absolute Patience

Ramadan is about overcoming base instincts and have patience.

(My newborn baby daughter, Yaslyn Inara relaxing by the sea.)

.

.

It’s not easy to withhold hunger and thirst, and to watch your behavior and grab at any opportunity you can to do good.

We are so used to eating and drinking whenever we want.

And also we rarely watch the things we say.

And we tend to be lazy or procrastinate.

So Ramadan forces us to hold back and in doing so, it requires patience on our part. Absolute patience. No two ways about that! 🙂

……………………………………

…………………….

……………….

Managing your finances is also about overcoming a basic instinct and have patience.

Humans are naturally inclined to instant gratification.

We want things NOW!

We hardly blink an eye eating out everyday or splurging on staycation / new bag / new gadget.

But the moment we need to set aside money for the future, most of us start coming up with all sorts of excuses.

The reason why we are adverse in saving up is because we don’t see its immediate benefit.

Although logically we know it’s to help us in the future, our base instinct is to enjoy things now.

So understand that in financial planning, you need to have absolute patience.

Be stronger than your basic instinct and commit yourself to save up or invest every month.

…………………………………………………….

………………………………..

……………………

Moderation

Ramadan is about moderation.

Everyday, after Azan Maghrib, I listened to the radio ads on Warna 94.2FM by Health Promotion Board.

It states that 1 out 6 Singaporean Malays from age 18-69 have diabetes.

This is a trend that is unhealthy and worrying.

As someone who loves to eat delicious food, enjoy sumptious buffets with beautiful, tantalising arrays of food,

I find Ramadan not only an opportunity for me to increase my Ibadah.

It is opportunity for me to watch my diet and eat moderately.

We eat heartily for suhoor, as we need energy to get on with the day.

And when we break for iftaar, the food we consume should be in moderation, enough for us to sustain our energy levels for the taraweeh prayers.

………………………………………..

………………………..

Our beloved Prophet Muhammad (Please And Blessings Be Upon Him) has taught us the formula for moderation when we eat our food. We should fill our stomachs with 1/3 of food, 1/3 of drink and leave 1/3 for breath.

Prophet Muhammad (Please And Blessings Be Upon Him) said: “No human ever filled a vessel worse than the stomach. Sufficient for any son of Adam are some morsels to keep his back straight. But if it must be, then one third for his food, one third for his drink and one third for his breath.”

[Ahmad, At-Tirmidhi, An-Nasaa’I, Ibn Majah – Hadith sahih]

(Myself Iftar with my family near Changi)

……………………………………

………………………….

……………….

Similarly, in managing our finances, we have to practice moderation.

Usually when I encounter very ambitious prospects who wants to start a shariah compliant investment plan with a big monthly contribution,

as a finanial planner, I will dig deep in their finance first.

How much are you earning?

What is your monthly expenses like? After deducting your monthly expenses, how much are you left with?

Do you have 3-6 months of emergency expenses set aside in your bank account?

You mentioned to me that you want to save $XXXX/month. Have you been saving $XXXX/mth for the last 6 months?

Yes? No? Why No?

If they are not ready, usually I would decline them as my client first and share with them strategies on how to accumulate money fast, over the short term period.

Of course, do it the shariah compliant way in Singapore.

Once they are financially stable, meet me again, and I share simple yet powerful financial strategies that I personally use to grow my wealth the shariah compliant way in Singapore.

My role, my relationship with them as a financial consultant is to help grow their investable assets and networth the shariah compliant way in Singapore.

And moderation is key.

Slow and steady always win the race. 🙂

(You can download a free report of me sharing how you can create your own personal networth statement and cashflow statement in less than 10 minutes even if you have no financial background. Click here. )

………………………………………….

……………………..

……………….

Act On Opportunities

Ramadan is about taking advantage of opportunities.

As mentioned, it’s a month where your deeds are doubled in reward and you’ll be forgiven for your sins if you’re sincere in your taubah. Let’s not be fools like the ones mentioned in the following hadith:

Abu Huraira (r.a.) related that Rasulullah (s.a.w) said: Many people who fast get nothing from their fast except hunger and thirst, and many people who pray at night get nothing from it except wakefulness (Darimi).

………………………………………………..

…………………………………..

…………………

Similarly, effective financial planning is about taking advantage of opportunities. You’re not going to be young forever.

For example, if you’re taking up a shariah compliant insurance plan, you pay less in terms of mortality charges if you’re in your early thirties as compared to when you’re in your forties. So instead of paying more in the future, why not start early and pay lesser yet still accumulate much more?

………………………………………..

……………………………..

………………………….

Talking about opportunities, a lot of you might be aware that in the year 2008 (subprime mortgage crisis)

which leads to global economic crisis (year 2009), I help a lot of my clients make money. They make a lot of money. Yet, I dont make much money.

(Myself and my fellow colleagues doing roadshows 10 years ago)

……………………………………………………………

……………………………………………

……………………………………….

At that time, I was 21 years old, just completed my 2 years army, and new to my job as a financial consultant.

In army, we only received about $500/mth, thus naturally I dont have much opportunity funds.

Nevertheless, I have financial knowledge (Diploma in Accountancy), and I managed to convince a lot of people to invest with me.

Yet, I dont have much to invest.

I remembered that Abang who came to me.

“Helmi…. Thank you so much lah for helping Abang make so much money via investment. Very good!

Btw, just want to check with you lah, how much percentage in terms of share of my profit, do you get??”

I answered, “Not a single cent”.

I was disappointed. I was sad for myself, yet happy for my clients.

I consoled myself by telling myself,

“Its okay Helmi. Now you are young. Start saving as much opportunity funds as possible. In investment, there are market cycles. In the future, when there is a market downturn, make sure you have a lot of money to capitalise on the OPPORTUNITY.”

Yes! Prepare and grab opportunities as it comes by! 🙂

Discipline and awesome time management

Ramadan teaches us to be disciplined. It’s not easy to go hungry and thirsty, and on top of that be on our best behavior.

This is only achieved through discipline, which comes from the taqwa (consciousness) of Allah.

In addition to that, Ramadan nurtures us to be discipline in how we manage our time.

We have to wake up earlier than usual to do our suhoor, then at night, our time is spent at taraweeh prayers.

So it’s very important for us to plan our day right, and this is where being discipline in managing our time well comes in. Otherwise, you’ll end up sleeping late and missing suhoor, or you’ll be too tired to do taraweeh because you were doing way too much during the day.

…………………

………….

………

(What I had for suhoor earlier, my protein shake and a drink)

………………………………………………………..

…………………………………..

…………………

Managing your personal finances is also about discipline.

A lot of people thought if someone earns a lot, he automatically becomes rich.

That is a myth. My experiences as a financial consultant tells me otherwise.

I have met someone who earns >$10,000/mth who cannot afford to get savings plan from me (always lapsing his policy and I have to chase for payment).

And at the same time, someone just earning $1,500 who has a few policies with me.

In fact, if you look at that same person, who earns >$10,000/mth facebook, you will be thinking,

“Woah! He is so lucky! So rich! Driving flashy cars and always travelling on expensive holidays all over the world”.

The beautiful part of being a financial consultant is that we dont look at you on the surface.

Expensive cars, branded goods to showcase etc2.

Those are good to have but superficial.

We look directly at your personal financial statements.

Anybody can start a savings or investment plan, but it takes character and utmost discipline to maintain it.

………………………

…………

..

Abstinence from haram stuffs

Similarly, when running a business or making money through investments, we have to ensure that it is Halal.

It is shariah compliant. Free from Riba. Maysir. And Gharar.

On the day of judgement, five basic queries that will be made to every being as per the following Saying of Prophet Muhammad (PBUH):

“The son of Adam will not pass away from Allah until he is asked about five things: how he lived his life, and how he utilized his youth, with what means did he earn his wealth, how did he spend his wealth, and what did he do with his knowledge.” (Tirmidhi)

Thus when a lot of people meet me, they realised I am a financial consultant that is different compared to majority of the other financial consultants in Singapore.

I have a different set of philosophies and principles .

When others advice their clients to take as much loans as possible as a form of leverage (as long as fulfil DSR), I advice my clients not to take interest bearing loans. Even if the interest rate is super low. It is because interest is riba. If you have it, clear it asap.

When others advice their clients on financial instruments that involved maysir and gharar, I advice my clients against that. No short selling of stocks. No speculative financial instruments.

And I advice my clients on how they can scrutinise their portfolio of investments via various shariah compliant screening methodologies like Dow Jones Islamic Markets, Securities Commission Malaysia etc2.

This is important because at the end of the day, we not only want to make money. We want the baraqah and Allah’s blessing together with it.

Amin. Insya’Allah.

……………………………………………………………………………………….

…………………………………………………………………..

…………………………….

…………..

Night Of Destiny

A Malay proverb says, “Kita hanya merancang, tuhan menentukan”.

I always share with my clients. In life, we can only plan.

Allah S.W.T. is the Master of Destiny.

As we are approaching the last 10 nights of Ramadan, we Muslims believe there is this one night known as Night of Destiny (Laylat al-Qadr).

On this special night the blessings and mercy of Allah are abundant, sins are forgiven, supplications are accepted, and that the annual decree is revealed to the angels who also descend to earth.

Make Tahajud prayers. Make Hajat prayers.

And when making doa to Allah S.W.T., I share with my clients, family and friends.

Dont make doa like,

“Ya Allah. Make me rich. Give me long life…. and the list continues”

Add these words. “Ya Allah. If this is good for me, good for my parents, good for my religion, grant me (what you wish)”

Put your trust in Allah S.W.T.

Biiznillah your doa will be maqbul. And if not, Allah S.W.T will replace with something better.

Insya’Allah. 🙂

……………………

………………

From a spiritual level, the Night Of Destiny is extremely powerful.

From the Imam of Makkah, he said for the last 10 nights of Ramadan,

1) If you donate $1 every night, and it falls under the night of destiny, it means as if you have donated every day for 84 years.

2) 2 rakaat of prayers every night, and it falls under the night of destiny, it means we pray every day for 84 years.

3) Read Surah Al-Ikhlas 3 times per night, and it falls under the night of destiny, it means we have read the entire Al-Quran everyday for 84 years.

(Translated from Ustazah Siti Nor Bahyah Mahamood facebook’s sharing, 18th June)

…………………………….

……………………………

………………

So that sums up my R.A.M.A.D.A.N formula.

And how you can learn the good principles of this beautiful month and apply it when managing your personal finance, the shariah compliant way in Singapore.

May Allah S.W.T accept our ibadah and good deeds that we performed in Ramadan. Insya’Allah! 🙂

p.s. By the way, if you wish to discover a simple & halal way to create a positive monthly cashflow and calculate your net worth for FREE, then pleaseclick here…

A certified financial consultant, Helmi Hakim has won praise for his patience, perseverance and practicality when solving his clients’ financial concerns. For more information on how you can manage your finances better, contact Helmi Hakim at 96520134.