Alhamdulillah… My wife and I landed safely in Athens a few days ago.

I would like to thank my clients, family and friends for helping me achieve this company’s incentive trip as a reward for my hard work in 2017. 🙂

……………………………….

………………….

Back to the topic…

The Malay proverb says, “Jauh perjalanan, luas pemandangan.”

It means when we travel more, we experience more on things that we’ve never experienced before.

While researching about Greece and their culture, assimilating with its people, I found some superb + AWESOME wealth habitsthat I feel, we should emulate them.

And I want to share them with you! 🙂

1. The Greeks Are Friendly And Approachable People

The Greeks are very friendly, cheerful and approachable people.

And then I found out… It is inherent in their culture dated many, many years back.

Xenia is the ancient Greek concept of hospitality.

It is the generosity and courtesy shown to those who are far from home honouring guest-friendship.

The rituals of hospitality created and expressed a reciprocal relationship between guestand hostexpressed in both material benefits (such as the giving of gifts to each party)

as well as non-material ones (such as protection, shelter, favors, or certain normative rights).

(Source:Wikipedia)

So that is why… when you see the Greeks, you can sense their warm, caring and sweet disposition.

To my mind, this kind of approachable disposition is important, especially when you run your own business.

When you run your own business, you have to work with people.

Your partners. Your staffs. Your customers! 🙂

Having such warm, caring and understanding disposition will make people LIKE you more.

They work hard because of you.

And in return, improve your company’s productivity and bottom line! 🙂

…………………………………………………..

………………………………

And oh yes!!! 🙂

Some small tips from me…. The Greeks love it especially if you as a foreigner try to speak their language. (Of course… Greek is the oldest written language in the world.

And Greek is one of the oldest language on Earth. Its spoken for over 3000 years!)

Say “Kalimera” instead of Good Morning.

Say “Efharisto”instead of Thank You.

Say “Efharisto poly” instead of Thank You Very Much.

You will see big proud smiles on their face.

To my mind, if you want to be good business people,

you have to be generous with your smile. Try to smile now! 🙂

Smile is also a sunnah of our beloved Prophet Muhammad (Peace Be Upon Him).

2. The Greeks have a healthy eating habits.

In sales, people with the highest energy wins.

And to have high energy, you must be healthy. You must be fit. You must be energetic.

My fitness coach always share with me that you are what you eat.

The Greeks have considerably one of the healthiest diet in the world.

This is because their diet is based largely around fruit and vegetables, wholegrains, fish, and a small amount of cheese and yoghurt.

Oh yes! They love olive oil.

(Fun Fact: They are over 120 million olive trees in Greece. Some being 7+ centuries.)

Honey.

Basically, all the healthy stuffs.

So, if you want to be a sales champion, a successful entrepreneur, you need to keep yourself fit!

You can adopt Greek diet lifestyle in your life too! 🙂

3. The Greeks are more frugal now.

Since their financial crisis, the Greeks are now more frugal with their spending.

Below are some findings according to a 2014-2015 study done by AUEB (Athens University of Economics and Business).

7 in 10 respondents said they have scaled down their expenses to mostly bare necessities.

96.4% of respondents will decide specifically on items to buy before heading to the shops. Of that, 60% would have already decided on the specific brand of products to buy (compared to just 49% in 2013).

…………………………………………………

…………………………………….

………………………

Personally, I think it’s a good idea to be very clear about the items we want to purchase before going to the malls.

Have a shopping list! 🙂

Once we have a clear and concise list at hand, there will be fewer chances of us spending on unnecessary items.

This brings to mind the constant battle of ‘Needs vs Wants’.

………………………………………………………………

………………………………………………

………………….

I will give a personal example.

From November 2017 till January 2018, Singapore was struck by the rainy season.

My wife helps me with our laundry and she noticed that our clothes took many days to dry – during that time.

It was inconvenient for us as we have a 10-month-old baby. Our baby changes clothes several times a day and needs freshly-cleaned clothes, towels and bibs every single day for school.

My wife had to buy new clothes and towels for our daughter to pack to school because the ones she washed took too long to dry.

She suggested buying a dryer and I was contemplating whether it was a ‘need’ or a ‘want’.

In the end, after witnessing several days of damp laundry not drying on time and as the unwashed pile of clothes gets bigger, we had no choice.

The dryer – which was more of a ‘want’ before the rainy season struck – became a ‘need’.

Simply put, ‘needs’ refers to necessitieswhereas ‘wants’ are items we desire to have.

To see how I apply the ‘Needs vs Wants’ concept to a different scenario, you can watch the video below. 🙂

This video refers to the common ‘Needs vs Wants’ battle which potential brides and grooms face when planning for a wedding.

.

4. The Greeks buy with cash.

When the Greeks go out for a meal, they will bring cash. That’s because credit cards and cheques are usually not accepted!

Interestingly, they will usually bring MORE CASH than necessary because it is considered embarrassing if they do not offer to pay for their friends’ meals as well. 🙂

Other than restaurants, many small shops only accept cash too.

This is good – as I’m a perpetual SUPPORTER of buying things with CASH!

Why?

This ensures that I will not accumulate debt – especially riba-based debts.

If you know me personally, you would know that I keep loans to a minimum.

At this moment, I only have 1 loan – my HDB housing loan, which I’m strategising to clear as fast as possible.

I equate ‘no loans’ with ‘freedom’. 🙂

And being free of riba-based loans (where possible) should also be the goal of most Muslims.

.

.

5. The Greeks would find many excuses to unite and celebrate.

The Greeks, they have this special concept known as “Kefi”.

Kefi has been described by various Greeks as meaning the spirit of joy. Passion. Enthusiasm. High spirits.Fun.In general, you love life. 🙂

Greeks do love festivities.

And they are always looking for an excuse to conglomorate, unite and celebrate.

These festivities bring families together.

Young and the elders meet. Share their story. Their life.

That is something to my mind, we should emulate on.

Whatever challenges we faced in life, persevere forward.

Always find time to strengthen the ukhwah, relationship with your family and friends.

I hope you learn something from my sharing.

My favourite past time is to learn about other peoples’ culture and embrace them if I find it compatible with our way of life.

If you will also like to discover aspects on how you can grow your wealth in Singapore,

combining the best in conventional finance, and the best in Islamic Finance.

I always believe 2 things will shape you to who you become in life. 1) The People Whom You Spend Most Time With Everyday 2) The Books You Read

Alhamdulillah. All Praises to Allah S.W.T. 🙂

A few days ago, I finished reading a New York Times bestseller book: Tools of Titans.

This 700-page book was written by Tim Ferriss who also wrote other successful books such as The 4-Hour Work Week.

I was attracted to Tools of Titans because it has nuggets of wisdom from over 113 world-class performers.

Billionaires.

Global icons.

High-achievers of the world.

My take is that if you want to be successful in whatever you do.

You have to model successful people.

People who have already achieved the results you desire.

And this book offers just that!!! 🙂

I like Tools of Titans because it is generously peppered with simple-to-copy actionable habits & routines done by these world-class achievers.

They are so simple that we can incorporate their habits into our lives – today. 🙂

……………………………………………..

………………………………………….

………………………….

For most of you whom have been following my blog posts dilligently.

You would have known that I am a financial consultant that specialise in helping Muslim families plan their finance, the shariah compliant way in Singapore.

As a practising financial consultant, I actively look out and find ways how to combine traditional, conventional business concepts.

And synthesize them together with shariah compliant best practices in the Islamic World.

In accordance to our glorious Quran and Hadith.

So here I present to you….

……………………………………………………………………………………………………………………………

…………………………………………………………………………………….

………………………………………………………………

…………

5 Shariah Compliant Hacks I Learn While Reading ‘Tools of Titans’ Book…

…………………………………………………………………..

…………………………………………….

………………………………………..

1. Taking Action is What Matters

There is a saying which goes: ‘Ideas are nothing. Doing is EVERYTHING.’

We can get any information we want using Google. Or borrow books from library.

Ask experts in their own field.

Or perhaps brainstorm them ourselves! 🙂

Yet, what is more IMPORTANT is what we do with the information. Taking action is what matters!

Jim Rohn, a motivational guru, mentioned in this book: “If you let your learning lead to ACTION, you become wealthy.” 🙂

Personally, I like attending seminars and I’ve been attending seminars since 10 years ago.

These seminars are not cheap – some cost thousands of dollars. When I’m at a seminar, I will give my 100% focus and implement strategies on the spot.

If I’m unclear about something, I will raise my hands and even speak into a mic in front of a large audience – just to clarify my doubt.

What happens after the seminar ends?

I apply the strategies ASAP and turn all my new knowledge into ACTION.

My actions have to lead to great results at work.

I will ensure that if I invest $1000 in a seminar, my results will DOUBLE, TRIPLE or QUADRUPLE the $1000 I spent.

In this book, Benjamin Disraeli’s quote: “Action may not always bring happiness, but there is no happiness without action” rings true for me. 🙂

……………………….

…………..

………

During my “Your Financial M.A.P.” session program, I share with my prospects on how they can clear their consumer loans FAST.

And at the same time, save their 3-6 months emergency expenses FAST.

I share with them.

Today, you come to me with money problems. Allah S.W.T. move your heart to meet me.

I never reach out to you. You are the one who come to me. The fact you meet me is a Qadr from Illahi.

I am just the asbab. The intermediary to share with you how you can solve your money problems.

If Allah S.W.T. shows you the way how you can solve your money problems, and you dont take action, you are the one who lose out.

Allah will not change the people, unless the people change what is in themselves.

Doa. Usaha( Action).And Tawakkal.

From an Islamic point of view, knowledge (ilmu) and action (amal) work hand in hand together.

………………………………….

……………….

…….. 2. The best investment is….in yourself.

According to Anthony Robbins, paying $35 for a 3-hour seminar (when he was 17 years old) was the turning point in his life.

He was reluctant to spend that money at first. Why?

Because he was a cleaner earning $40 a week at that time!

But he got clarity and direction with that $35 – which was priceless.

For me, although I am a finance degree holder, and considered fairly experience in my line of duty,

I continue to invest in myself.

I bought books. I took more Islamic Finance certifications.

Undergo more business development courses. More personal development seminars.

I travelled regularly.

To Kuala Lumpur.

To gulf countries like Oman, Dubai. To all parts of the world.

To seek fresh new ideas.

And to seek mentors and learn from the best in the industries.

To me, once you stop learning, you stop earning.

The best investment you can do is… investing in yourself.

Even Warren Buffett took a public speaking course when he was 20 years old.

Warren Buffett may be a legend in the investment field, but he is still a firm believer of investing in himself.

……………………………………

…………………..

…………

The idea of continually upgrading ourselves with ilm (knowledge) is synonymous with Islam.

We educate ourselves to what is right. And what it wrong.

How do we know what is right (Amar) and what is wrong (Maaruf)?

Through guidance from the right mentors and acquiring ilm (knowledge) by reading.

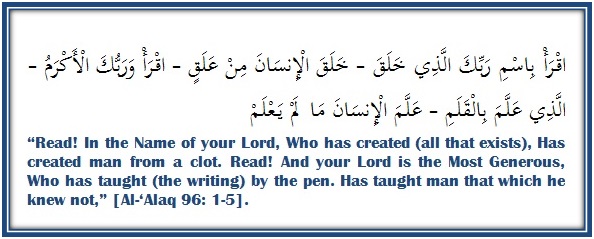

When our beloved Prophet Muhammad (Peace Be Upon Him) received his first revelation in the Cave of Hira’ through the angel Jibril (Gabriel), he was asked to read (Iqra’).

………………………………………………………………………….

………………………………………………………………

…………………………

……………………………………………………..

………………………………………………

…………………………….

The first words that were revealed to our beloved Prophet Muhammad (Peace Be Upon Him)

were ‘Iqra’ (Read).

and then, Alhamdulillah, our beautiful Deen, Islam was established.

…………………………………………………

…………………………………

………………….

I pray to Allah (SWT) to help us all develop a love for reading beneficial booksand increase us in beneficial knowledge. Amin… Amin… Insya’Allah! 🙂

‘Allaahumma ‘innee ‘as’aluka ‘ilman naafi’an, wa rizqan tayyiban, wa ‘amalan mutaqabbalan.’

(O Allaah, I ask You for knowledge that is of benefit, a good provision, and deeds that will be accepted)

(Recite in Arabic upon rising in the morning)

3. ‘Put the big stones in first’

This quote is from Kaskade, a five-time Grammy-nominated musician.

This quote means: to give time and attention to the important things in our lives first.

For example, my ‘big stones’ (or important things in my life) are my family and my work.

(One of the most important things in life. My family.)

……………………………………………………………….

………………………………………………………….

…………………………………….

Imagine holding a glass jar in your hand.

And you have sand, small stones and big rocks on a table next to you.

When we put the small stones and sand in the jar first, the big rocks can’t get in it.

But when we fill the jar with the big rocks first, the smaller rocks and sand can find little corners and spaces to fit in.

Everything fits in the end!

This metaphor means: to block out time every day for the important things (the ‘big rocks’), first.

The little less-important tasks will be scheduled around the ‘big rocks’.

For work, the ‘big rocks’ should be tasks which bring you closer to a big work-related goal.

Prioritise what matters 🙂

……………………………..

……………..

………..

4. Conquer Your Fear with 4 Simple Yet Powerful Questions

Most people will choose unhappiness over uncertainty – according to Tim Ferriss.

Many of us are scared of uncertainty and failure.

If you want to try something very much.

Yet, you are too scared to do so.

You can CONQUER that fearusing these 4 simple yet POWERFUL questions.

They are…

• What is the absolute worst thing that could happen if you did what you are considering?

• What steps can you take to repair this damage and get everything under control?

• What is costing you – financially, emotionally and physically – to postpone this action?

• Do you know anyone who is less qualified than you who has done this before and pulled it off?

……………………………….

…………………….

……………

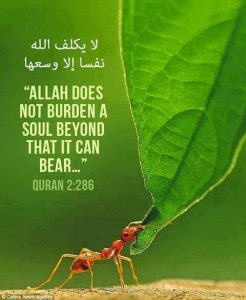

When I am confronted with “challenges” in life.

OR when I am presented with an opportunity that sends butterflies to my stomach,

I recalled this ayah.

Surah Al Baqarah, Verse 286 in our holy Quran. “Allah does not burden a soul, beyond that it can bear.”

And then, I do my level best to CONQUER that fear using these 4 simple yet POWERFUL questions.

• What is the absolute worst thing that could happen if you did what you are considering?

• What steps can you take to repair this damage and get everything under control?

• What is costing you – financially, emotionally and physically – to postpone this action?

• Do you know anyone who is less qualified than you who has done this before and pulled it off?

………………………………………………..

……………………………………………

…………………..

After answering those questions, usually I will feel good.

More confident. MORE focused. And MORE EXCITED!

And I start to draft out my plan. Because I know that 80% of success in any endeavour boils down to preparation!

And that is how I overcome challnges and prepare myself 101% to succeed in whatever opportunities presented to me! Insya’Allah! 🙂

…………………………………………………………….

………………………………………..

…………………………

5. Long term goals need long term focus

When we are going after our long-term goals, frustrations will crop up along the journey.

Some people thought, successful people have it easy.

Chicken feet for them. Everything goes as planned. No challenges.

Easy peasy!

haha! Not true!

Let me give you a real life example that happened earlier this morning! 🙂

……………………………………………………

…………………………………..

……………………

For the past few months, I have been studying brands worldwide and was inspired to have my own uniform. Takaful.sg set of uniform! 🙂

I want to look good, carry my brand proudly and appear well-dressed in front of my clients.

Thus I spent hours shopping for some good quality shirts.

And sent them to have my logo printed at a printing shop.

Was told that the whole process will take 3 weeks. I waited for over a month.

No calls. No SMS. No whatsapp msges.

Then I decided to pay them a visit.

To my disappointment, when I came down to collect my shirts, the logo was not printed as expected!

It looks amateurish, like plastic stickers pasted on the shirts!

I felt disheartened. Angry. Sad.

Disillusioned.

Takaful.sg is my baby. Is my brand!

It’s what I have been working so hard, day and night to build it to what it is today!

How can they haphazardly smack my brand???!

Then, I recalled what entrepreneur and renowned gymnastics coach,Christopher Sommer (Coach Summer) said in the book, “Impatience in dealing with frustration is the primary reason that most people fail to achieve their goals.”

Facing frustrations is part of the path towards excellence! 🙂

I told myself, we have to stay focused for the long-term if we want to achieve our long-term goal.

We can’t be beating ourselves up for small bumps along the journey.

The path to success is never straight! 🙂

“Learn and appreciate the process,”mentioned Coach Sommer.

……………………………………

……………………

………….

There you have it 🙂

5 Shariah Compliant Hacks Found in ‘Tools of Titans’ Book which not many peeople are aware of! 🙂

I have learnt much, much more than just 5 Hacks from this book.

Every time I open this 700-page book, I will come across a nugget of valuable advice which I did not notice before.

Which other self-help book would you recommend? 🙂

……………………………………………………………………………………………………….

…………………………………………………………….

………………….

If you like to integrate more POWERFUL STRATEGIES in your life.

If you will also like to discover aspects on how you can GROW YOUR WEALTH, the shariah compliant way in Singapore, you can always whatsapp/sms me at 96520134to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

I make myself available for 5 consultations per week.

Today is the 12th day of the Islamic month of Rabi’ al-awwal, which is our beloved Prophet Muhammad (Peace Be Upon Him)’s birthday.

We, Muslims believe that Prophet Muhammad (Peace Be Upon Him) is the last and final messenger of God.

Since young, when I read the seerah of our beloved Prophet, I am amazed at how much that we can learnt from him.

And today, I will like to touch specifically on 7 Good Business Habits of our beloved Prophet Muhammad (Peace Be Upon Him).

……………………………………..

…………………

…………

1) Trustworthy (Al Amin)

Our beloved Prophet Muhammad (Peace Be Upon Him) was involved in trade since his early adulthood.

And he quickly gained the title Al-Amin (the Trustworthy).

Then he came under the employment of a well known businesswoman named Khadija bint Khuwaylid.

He was recommended to her by his uncle, Abu Talib.

“If you had requested this for the sake of a loathed stranger, I would have agreed. How can I refuse when it is for an honorable acquaintance?” she had said to Abu Talib, for she was also familiar with Rasulullah’s reputation.

.

.

In Islam, we learnt that 9/10 of sources of rezeki (income) can be derived from business activities.

And in running our own business, we also seek the baraqah and redha from Allah S.W.T.

To get baraqah and redha from Allah S.W.T. in business, we need to have good character. We need to be Trustworthy.

It’s very easy to be greedy in trade, which is why a lot of cheating, cutting corners, riba and exorbitant pricing happen.

So if you want to seek baraqah and redha from Allah S.W.T., follow the steps of our beloved Prophet Muhammad (Peace Be Upon Him).

Being transparent, truthful and trustworthy is the first step to gain the trust of your clients and running a successful business.

.

.

2) Always give salam to your customers/prospects

Abdullah ibn Amr (may Allah be pleased with both) narrated that a man asked the Messenger of Allah (Peace be Upon Him) regarding which aspect of Islam was better.

Prophet Muhammad (Peace Be Upon Him) replied:

“That you feed (others), say the greeting of salaam to those whom you know and those whom you don’t know”.

Start with, “Assalamualaikum” greetings with your clients and even with your prospects who you don’t know them personally.

“Assalamualaikum” means “Peace Be Upon You”.

.

.

3) Smile

Smile is sunnah of Prophet Muhammad (Peace Be Upon Him).

Abdullaah ibn Haarith said, “I’ve never came across a person who smiled as much as Prophet Muhammad. Prophet Muhammad regarded smiling to a brother as an act of charity.”

Smiling is like a magnet that attracts rezeki for business people.

The more we smile, the more people will like us.

And we will also attract positive vibes and cheerful customers in our business. Insya’Allah. 🙂

.

.

.

4) Avoid appointments during solat prayer time

“Verily, As-Salaah (the prayer) is enjoined on the believers at fixed hours”

[al-Nisa’ 4:103].

.

.

Personally, I do my best to avoid my financial planning consultations during solat prayer time.

Subuh @ 5.28am

Zuhur @ 12.53pm

Asar @ 4.16pm

Maghrib @ 6.54pm

Isyak @ 8.07pm

.

.

.

5) Doa

Prophet Muhammad (Peace Be Upon Him) said “Dua is the essence of Ibadah (worship).” (HR At-Tirmidzi)

.

.

As Muslims, we believe that there is no middle man between God and his slaves. Any help we need, be it in business or life, we are to call unto him directly.

.

.

God tells us:

“And your Lord says, Call upon Me; I will respond to you.” Indeed, those who disdain My worship will enter Hell [rendered] contemptible.” Quran 40:60

.

.

And these are the 3 most mustajab time to make doa.

The Last Third Of The Night

Abu Hurairah (RA) narrated that Allah’s Messenger (SAW) said:

‘In the last third of every night our Rabb (Cherisher and Sustainer) (Allah (SWT)) descends to the lowermost heaven and says;

“Who is calling Me, so that I may answer him?

Who is asking Me so that may I grant him?

Who is seeking forgiveness from Me so that I may forgive him?.”‘ [Sahih al-Bukhari, Hadith Qudsi]

While Prostrating

Abu Hurairah (RA) narrated that Allah’s Messenger (SAW), said: ‘The nearest a slave can be to his Lord is when he is prostrating, so invoke (supplicate) Allah (SWT) much in it. [Muslim, abu Dawud, an-Nasa’i and others, Sahih al-Jami #1175]

Between Adhan and Iqamah

Anas (RA) narrated that Allah’s Messenger (SAW) said: ‘A supplication made between the Adhan and Iqama is not rejected.’

[Ahmad, abu Dawud #521, at-Tirmidhi #212, Sahih al-Jami #3408, an-Nasai and Ibn Hibban graded it sahih (sound)]

.

.

.

6) The best humans bring the most benefit to other human beings

Prophet Muhammad (Peace Be Upon Him) said, “The best of people are those that bring most benefit to the rest of mankind.” [Daraqutni, Hasan]

That is why I always advocate that in whatever business or profession we do, continue to upgrade ourselves.

Perfect the effectiveness and efficiency of our systems. The quality of our service.

So as to provide the best value, the optimal benefit for our clients, our community and the rest of mankind. Insya’Allah. 🙂

.

.

.

7) Understanding Muamalat and Avoid all forms of riba

As business people, when we study Muamalat, we need to pay close attention especially when it comes to practising business transactions.

Muamalat – Actions among men: This refers to how people interact with each other in their day-to-day affairs and dealings with people. This includes such things as trade, partnerships, laws, … as well as Islamic Finance.

Unlike Ibadat, a general principle that applies to Muamalat is that everything is allowed, except for what has been prohibited.Therefore as business people, we need to know the prohibitions. (Explanation adapted from Almir Colan)

Example:

– Prohibition of riba, maysir and gharar

…………………………….

………………….

……………….

As you can see above, there are many things we can learn from our beloved Prophet Muhammad (Peace be Upon Him) when it comes to running our business.

In business, cashflow is king. Having money on hand is important.

Thus, if you will also like to discover aspects on how you can save, accumulate and grow your money the shariah compliant way in Singapore, you can always whatsapp/sms me at 96520134 to schedule a FREE consultation.

Or perhaps click here to schedule an appointment.

Alhamdulillah… My facebook page is up after hiatus for about a year.

Please help to like my page here, www.fb.com/helmihakim.fp/ and then click the button, “See First”.

I will be creating live videos in the future, sharing specifically how you can save, accumulate and grow your money the shariah compliant way in Singapore.

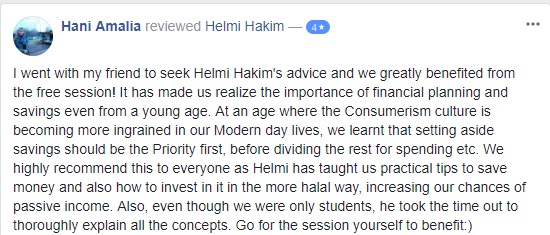

Attached are some testimonials for my signature programs, “Unlock Your Money” session

and also “Your Financial M.A.P” session.

If you want want to arrange a complimentary one hour private financial consult session (valued at $500) with me at my Tampines Point office, whatsapp me directly at 96520134.

Consultations after 8pm will be at Punggol Waterway Coffeebean.

I am fully booked till end of this year, and can only accommodate 3 additional sessions per week, starting 20th November 2017 till year end. If you are interested, reserve your FREE session now!

See you! Insya’Allah! 🙂

A certified financial consultant, Helmi Hakim has won praise for his patience, perseverance and practicality when solving his clients’ financial concerns. For more information on how you can manage your finances better, contact Helmi Hakim at 96520134.